Summary

-

2017 saw China transcending from a deficit economy into a surplus one. Per-cap GDP will soon leapfrog the threshold of USD 10,000. The dominant strategy of scale competition at all costs, as seen in all walks of life in China, will soon give way to quality competition. The “Three Critical Battles” accentuate the shift from “Is there enough?” to “Is it good enough?”

But consensus is still biased by unthoughtful sell-side research produced by the mountain of low-cost fresh graduates, as evidenced by the extremely euphoric market sentiment.

Near-term caution is warranted

. Our contrarian view on small caps to recover in 2018 has been met with scorns. But small caps in Hong Kong have rallied, while in mainland they have been traversing along a rising long-term trend line.

Small caps, as measured by the CSI500 index, have larger market cap than the so-called "emerging blue chips" measured by the A380 index, similar earning quality as the A50 big caps, and have significantly outperformed the A50 index since 2005. Value investing, as it is defined by the crowd buying big caps, has never really worked in China. And the so-called “liquidity premium” attached to big caps can only be defined during the time of crisis, and can induce heavier sell-offs because of the urge to raise cash to meet redemption.

Consensus has converged on growth outlook, and is converging on inflation outlook. As such, they are largely priced in, and are unlikely to be the alpha factor - especially growth. It is the changes in market trading structure, rather than inflation, that are keeping bond yields elevated. As the Fed curtails its balance sheet, an indiscriminate price taker on bond trading is disappearing. In China, commercial banks, who trade and hold the bulk of China’s bond market, are restricted by new regulations to deleverage. If growth could surprise consensus, growth assets such as small caps, EM and commodity should outperform. If not, and if inflation calms, bonds should recover. Otherwise, all bets are off.

This is the last report before the Year of the Dog. We thank you for your support all these years. In particular, we thank you for voting us as the Best Strategist and the Best Economist, and 12 top three awards in total, in the 2017 "Asia Money" Instiutional Survey. We wish you and your family a Happy New Year!

这是今天报告的英文原版《

The Year of the Dog: Lessons from 2017

》,感谢阅读。中文翻译版将稍后发出。视频是2017年11月与第一财经《首席对策》对2018年展望的专访。请点击本文最下方的“

阅读原文

”查阅原文文字内容。

--------------------------

“No discussion of the interrelations of stock prices and business conditions would be complete without emphasizing that in the clash of speculative forces on the exchange, the emotions play a part which is not paralleled in the normal processes of commerce and industry.

The golden mean is non-existent in Wall Street, because of the speculative mechanism does all things to excess; even the reactions from the heights of phantasy and from the depths of despair are accompanied by convulsions which are distinct from the calmer tenor of business.

Those who seek to relate stock movements to the current statistics of business, or who ignore the strongly imaginative taint of stock operations, or who overlook the technical basis of advances and declines, must meet with disaster, because their judgment is based upon the humdrum dimensions of fact and figure in a game which is actually played in a third dimension of the emotions and a fourth dimension of dreams”.

– Ten Years of Wall Street, Barnie Winkleman

Lessons from 2017

Quality rules over quantity

. 2017 may have spelt the beginning of the end of China’s competing on sheer bulk. Before, the dominant competitive strategy for China is scale: a growth-centric economic model with little regard of quality; cheap exports driven by an undervalued currency; and a domestic consumer market that closely resembles the orthodox model of perfect competition.

Even on more micro level, the mantra of massive scale competition is palpable. Small and mid-sized banks expanding their asset size off-balance-sheet through regulation loopholes. Many of them now have a bank on balance sheet, and another off. Movie studios, internet retailers, microblogs et al. have resorted to paying to paint a facade of box-office hits, hot sales and zombie fans and readership.

Sell-side research has piled on armies of fresh graduates from “211” universities to produce voluminous but thoughtless research. As such, biased consensus at times is quick to root, germinate and blossom to be nearly immutable. At its extremes, parts of the society are like an entity built upon Gresham’s Law that allows bad money to proliferate.

Regulators are quick to take actions. And they are decisive this time. For instance, the growth of shadow banking has been curbed, with new rules being released almost on a weekly basis, at the cost of epic waves of bond market sell-off. The paid search functions on microblogs and social media promoting uncouth fake news have been censored.

The government will “

prompt the finance industry to focus on their main business and make their services accessible to small and micro businesses, strengthen their ability to serve the wider economy and stop them being distracted from their intended purpose

”.

As such, the finance industry will go through the hardship of deleverage in the coming years, and will most likely face its own supply-side reform. Indeed, the Three Critical Battle highlighted in the official’s speech at the WEF this year, namely

1) preventing and resolving the major risks, 2) targeted poverty reduction, and 3) controlling pollution

, suggest that quality will rule over quantity. The government’s work focus is shifting from “

Is there enough?

” to “

Is it good enough?

”

Euphoric market sentiment suggests caution on near-term trading

. While the end of scale competition has begun, market consensus for now is still swayed by biases. One sign hinting at partial consensus is that market sentiment, measured by our proprietary sentiment indicator, has shown unfettered euphoria (

Exhibit 1

). Our sentiment indicator, albeit not infallible, has an excellent track record. For instance, it had pinpointed the market peak in October 2007 when the Shanghai Composite was above 6000 points, and again in June 2015 when the Composite was above 5000 points - two of the biggest stock market bubbles in recent history.

Exhibit 1: Market sentiment has reached extreme, suggesting near-term trading caution.

While we think economic outlook remains sound, market sentiment at such extremely elated level suggests near-term caution for traders. We need to reassess when to rebuild positions after the short-term market excess dissipates.

Non-Consensus Views

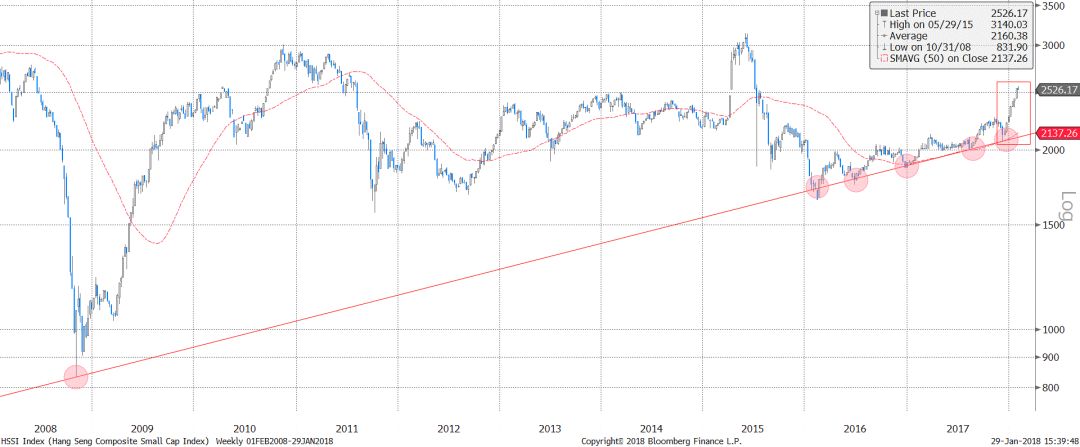

Chinese small caps are on a long-term rising trend

. 2017 is the first time in more than a decade when large caps rose while small caps fell. The underperformance of small caps has been so extreme and extended that most have relinquished hopes. In our outlook report titled

“View from the Peak

” on December 4, 2017, we highlighted small caps, as measured by the CSI500 Small-Cap index, should come back after a dismal year as one of our contrarian calls. Since our report, the stretched strength in the A-share big caps has deafened even the most accommodative ears.

Exhibit 2: The long-term rising trend line of mainland/HK small caps. HK small caps have started to surge (lower panel).

But the Hong Kong small caps have started to surge since our report (

Exhibit 2

). They have indeed outperformed the Hong Kong big caps as denoted by the Hang Seng Index. The A-share small caps have also risen. Although they have failed to outperform the big caps, they continue to bounce off their rising long-term trend line. Their valuation is perching on the long-term trend line as well (

Exhibit 3

). The divergence of performance between A-share and Hong Kong small caps suggests entrenched biased consensus in the domestic A-share market. It will take time for the domestic market to come to terms with our contrarian view.

Exhibit 3: The valuation of China small caps is perching on a rising long-term trend line.

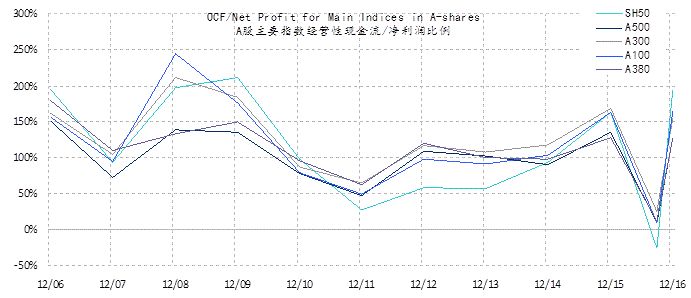

Small caps’ earning quality is just as good as that of large caps; value investing has never worked in China.

Many equate buying big caps as value investing, and hail the outperformance of big caps in 2017 as the return of value investing.

Exhibit 4: A-share small caps’ earnings quality is as good as that of other larger-cap indices.

Since the inception of the CSI500 Small-Cap index in 2005, its cumulative performance of has been more than two to three times of that of the SSE50 A50 Big-Cap index. Further, after taking out banks and other capex-intensive industries, CSI500’s quality of earnings, as measured by the ratio of Operating Cash Flow to Net Profits (OCF/NP), tracks that of SSE50 very closely. And there is no discernable statistical difference (

Exhibit 4

). And the average market cap of the CSI500 index companies is around ~RMB 16bn, as compared with ~RMB 14bn of the SSE380 index companies, a.k.a. the "emerging blue chips".

In short, the quality of earnings, the cumulative return over the years and the market caps of the CSI500 index companies are just as good as, or at times even better than those of the SSE50 index companies.

There is also a school of thoughts that believe big caps should be bought for their “liquidity premium”. We believe that these pundits have confused trading volume with liquidity, which should be defined at the time of crisis. When the chance of a crisis is still low due to the regulators resolve to ward off systemic risks, the regime to value stocks on liquidity is off. We also note that assets with liquidity tend to be sold off during crisis to raise cash, and thus will suffer even more, as seen in the Mexican plunge during the Argentina Crisis in the early 90’s. Be careful what you wish for.

Inflation or not, bond yields are difficult to decline for now because of tightening regulation