本文的作者是纽约大学金融系教授Aswath Damodaran,号称“华尔街太傅”,目前在NYU的商学院教授估值课程,是华尔街最热门的教授之一,为华尔街培训了大量的精英。本文作者主要讨论了从财务比率看全球股票定价。

When looking at how stocks are priced and especially when comparing pricing across stocks, we almost invariably look at pricing multiples (PE, EV to EBITDA) rather than absolute prices.

That is because prices per share are a function of the number of shares and are, in a sense, almost arbitrary. Before you respond with indignation, what I mean to say is that I can make the price per share decrease from $100/share to $10/share, by instituting a ten for one stock split, without changing anything about the company.

As a consequence, a stock cannot be classified as cheap or expensive based on price per share and you can find Berkshire Hathaway to be under valued at $263,500 per share, while viewing a stock trading at 5 cents per share as hopelessly overvalued.

在看股票是如何定价时,尤其是对不同股票的价格进行对比时,我们几乎会都会去看各种指标(PE, EV 和 EBITDA),而不会去看绝对价格。因为股票的每股价格由股票数量决定,在某种程度上,这是可以投机的。

先别急着生气,我这么说的意思是,只要把1只股拆分成10只股,股价就能从100美金掉到10美金每股,但是公司还是同一家。所以,我们无法根据每股价格的高低来判断股票是便宜还是昂贵,你会发现股价高达263,500美金的伯克希尔哈撒韦也被低估过,你也会绝望的发现交易价格才5美分的股票也还是会被高估。

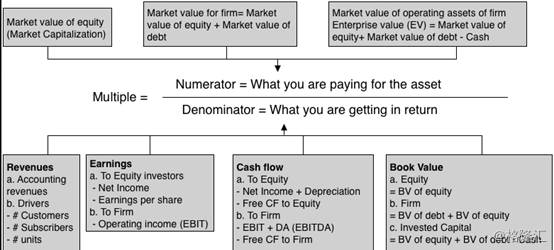

The process of standardizing prices is straight forward. In the numerator, you need a market measure of value of equity, the entire firm (debt + equity) or the operating assets of the firm (debt + equity -cash = enterprise value). In the denominator, you can scale the market value to revenues, earnings, accounting estimates of value (book value) or cash flows.

让价格标准化的过程很简单。把分子设为公司所有者权益、或整个公司(负债+所有者权益)的市场价值,也可以是公司的经营性资产价值(负债+所有者权益-现金=企业价值)。把分母设为营收,净收入,价值(账面价值)或者现金流的会计估值。

图片注释:

作者认为衡量股票价格是否“合理”的指标应该是:你为企业的资产支付的价格÷你所得的回报收益。分子可以为以下三项:(1),企业所有者权益的市场价值(市值);(2)企业的市场价值,也即企业所有者权益的市场价值+负债的市场价值;(3)企业经营性资产的市场价值,即所有者权益市场价值+负债的市场价值-现金。 分母可以是以下四项:营收,净收入,现金流,账面价值。

As you can see, there is a very large number of standardized versions of value that you can calculate for firms, especially if you bring in variants on each individual variable in the denominator.

With net income, for instance, you can look at income in the last fiscal year (current), the last twelve months (trailing) or the next year (forward). The one simple proposition that you should always follow is to be consistent in your definition of multiple.

如你所见,企业的价值有很多个标准化的计算版本,尤其是在分母的各个变量中再引入可变因素时更是如此。比如净利润这一项,你可以用上一财年的净利润(本期收益),也可以是过去12个月的收益(持续收益),或者是下一年的收益(预期收益)。需要遵守的一个简单的原则就是你给这个指标下的定义得始终保持一直。

The "Consistent Multiple" Rule: If your numerator is the market value of equity (market capitalization or price per share), your denominator has to be an equity measure as well (net income or earnings per share, book value of equity.

For example, a price earnings ratio is consistent, since both the numerator and denominator are equity values, and so is an EV to EBITDA multiple. A Price to EBITDA or a Price to Sales ratio is inconsistent, since the numerator is an equity value and the denominator is to the entire business, and will lead to conclusions that are not merited by the fundamentals.

“指标一致性”原则:如果分子是所有者权益的市场价值(即市值或者每股股价),分母就必须也按照所有者权益的方法计算(净利润,或者EPS或者是股权的账面价值)。例如,P/E这个指标符合“一致性”原则,因为分子、分母都是股权价值,EV(企业价值),EBITDA( 未计利息、税项、折旧及摊销前的利润)都是这类指标。股价/EBITDA,或者股价/营收都是不符合“一致性”原则的指标,因为分子指的是股权价值,分母是整个企业的,这回导致结果和基本面不符合。

Pricing – A Global Picture

价格-全球展图

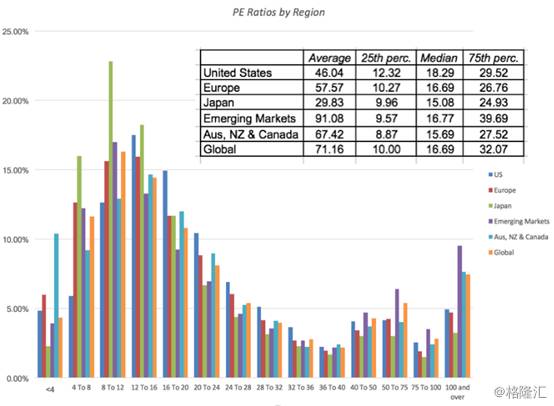

To see how stocks are priced around the world at the start of 2017, I focus on four multiples, the price earnings ratio, the price to book (equity) ratio, the EV/Sales multiple and EV/EBITDA. With each multiple, I will start with a histogram describing how stocks are priced globally (with sub-sector specifics) and then provide country specific numbers in heat maps.

为了看看在2017年初全世界的股票价格如何,我关注了四个指标,市盈率(P/E),市净率(P/B),企业价值(EV)/营收,还有企业价值(EV)/EBITDA。我们以几张展示了全球股票价格的柱状图依次谈谈每一个指标,然后在热量地图上展示具体一些国家的股票价格。

PE ratio

市盈率

The PE ratio has many variants, some related to what period the earnings per share is measured (current, trailing or forward), some relating to whether the earnings per share are primary or diluted and some a function of whether and how you adjust for extraordinary items.

If you superimpose on top of these differences the fact that earnings per share reported by companies reflect very different accounting standards around the world, you can already start to see the caveats roll out. That said, it is still useful to start with a histogram of PE ratios of all publicly traded companies around the world:

市盈率这个指标有很多变量,有些跟每股收益(EPS)的计算时间段有关(本期收益,持续收益,预期收益),有取决于是普通EPS还是稀释后的EPS,有些取决于你如何调整非经常性项目。

除了这些变量,如果你还认识到公司披露出的EPS反映的是世界各地各不相同的会计准则,那么你就能看到危险信号出现。也就是说,从研究世界各地上市公司的P/E比率着手是有意义的:

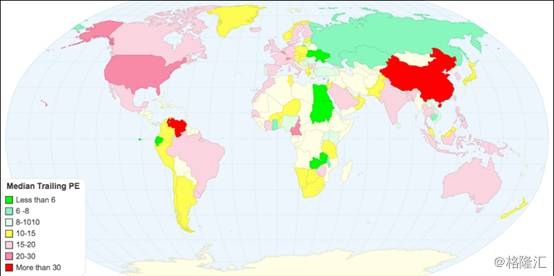

Note that of the 42,668 firms in my global sample, there were only 25,493 firms that made it through into this graph; the rest of the sample (about 40%) had negative earnings per share and the PE ratios was not meaningful. While the histogram provides the distributions by regional sub-groups, the heat map below provides the median PE ratio by country:

留意:在全球42668家样本公司中,只有25493家被录入上图中;其它的样本的(大约有40%的公司)EPS为负数,所以其P/E并无意义。上面这幅柱状图展示了按照地域划分P/E分布,下面的热量图展示了各个国家的P/E中位数。

I mistrust PE ratios for many reasons. First, the more accountants can work on a number, the less trustworthy it becomes, and there is no more massaged, manipulated and mangled variable than earnings per share. Second, the sampling bias introduced by eliminating a large subset of your sample, by eliminating money losing companies, is immense. Third, it is the most volatile of all of the multiples as it is based upon earnings per share.

我不信任P/E指标的原因有很多。首先,越是会计能动手脚的数字,这个数字的可信度就越小,没有什么变量比EPS还容易被操控篡改的了。其次,由于消除了大部分样本和亏损的公司之后,形成了极大的样本偏差。最后,由于P/E指标的基础是EPS,所以P/E是所有指标里面最不稳定的。

Price to Book

市净率

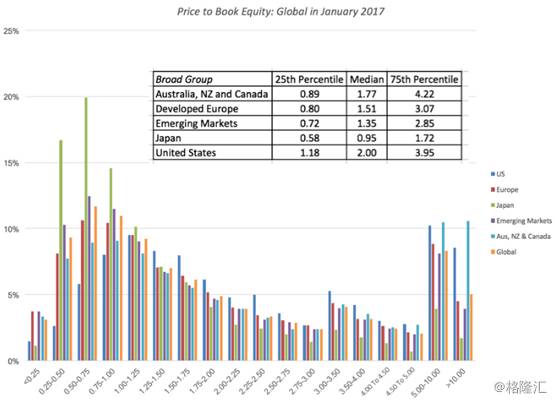

In many ways, the price to book ratio confronts investors on a fundamental question of whether they trust markets or accountants more, by scaling the market’s estimate of what a company is worth (the market capitalization) to what the accountants consider the company’s value (book value of equity).

The rules of thumb that have been build around book value go back in history to the origins of value investing and all make implicit assumptions about what book value measures in the first place. Again, I will start with the histogram for all global stocks, with the table at the regional level imposed on it:

很多时候,市净率都将投资者置身于这样一个本质问题当中:从市场对公司的估值(市值),到会计认为公司值多少,投资者究竟是相信市场多一点,还是相信会计多一点。这一围绕市净率形成的首要规则可以追溯到价值投资的起源时期,大家对账面价值最开始衡量的是什么进行含糊的假设。我们还是以一张全球股票的柱状图开始,另附上一张地域图表。

The price to book ratio has better sampling properties than price earnings ratios for the simple reason that there are far fewer firms with negative book equities (only about 10% of all firms globally) than with negative earnings. If you believe, as some do, that stocks that trade at less than book value are cheap, there is good news: you have lots and lots of buying opportunities (including the entire Japanese market). Following up, let’s take a look in the heat map below of median price to book ratios, by country.

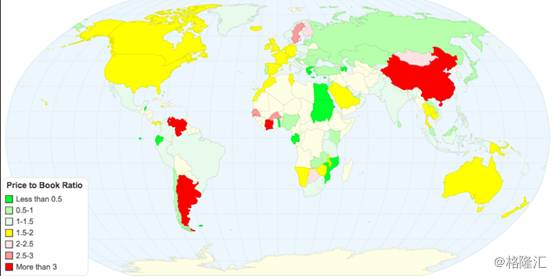

由于账面所有者权益为负的公司极少(全球只有10%),所以市净率的样本公司数据比市盈率的要多。跟有些人一样,如果你觉得股价的交易价格低于其账面价值就算便宜了,那么有一个好消息:你有十分十分多的买入机会(整个日本股市都涵盖其中)。现在我们看看下面的按国家划分的市净率热量分布地图。

Pausing to look at the numbers, note thecountries shaded in green, which are the cheapest in the world, at least on aprice to book basis, are concentrated in Africa and Eastern Europe, arguably among the riskiest parts of the world. The mostexpensive countries are China, a couple of outliers in Africa (Ivory Coast andSenegal, with very small sample sizes) and Argentina, a bit of a surprise.

我们暂停一下看看图中的数字,注意:绿色标记的地域其股价在世界范围内是最低的,至少基于市净率来看是这样,这部分区域主要集中在非洲和东欧,这些地方可以说是世界上风险最大的地区。股价最高的地方是中国以及非洲大陆外缘的一些地方(像象牙海岸和塞内加尔这些地方,样本量很小),还有阿根廷,有些出人意料之外。

EV to EBITDA

EV/EBITDA比率

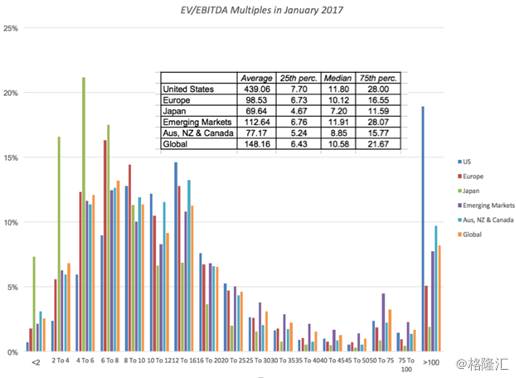

The EV to EBITDA multiple has quicklygrown in favor among analysts, for some good reasons and some bad. Among thegood reasons, it is less affected by different financial leverage policies thanPE ratios (but it is not immune) and depreciation methods thanother earnings multiples.

Among the bad ones is that it is a cash flow measurebased on a dangerously loose definition of cash flow that works only if youlive in a world where there are no taxes, debt payments and capitalexpenditures laying claim on those cash flows.

The global histogram of EV toEBITDA multiples share the positive skew of the other multiples, with the peakto the left and the tail to the right:

EV/EBITDA比率在分析师中的迅速走俏,其中有好有坏。好在于/EBITDA相较于P/E而言受到财务杠杆策略的影响较小(但绝非完全免疫),较之于其它指标而言,EV/EBITDA受到不同折旧方法的影响也较小。

不好在于,这个现金流计算方法是基于对自由现金流为危险且松散的定义之下,只有在一个没有对自由现金流征收赋税、没有负债和资本开支的世界里才有用。EV/EBITDA的全球分布柱状图和其它比率有正相关走势关系,左边是高峰,右边是尾部。

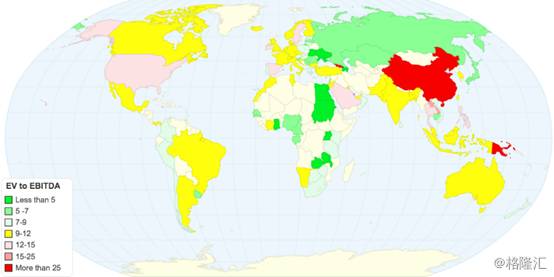

Again, there will be firms that had negative EBITDA that did not make the cut, but they are fewer in number than those with negative EPS. Looking at the median EV to EBITDA multiple by country in the heat map below, you can see the cheap spots and the expensive ones.

同样,由于没有减税,也有EBITDA为负数的企业,但是这类企业还是比EPS为负的企业要少。从下面EV/EBITDA中位数的国家分布图可见哪些地方的股价便宜,哪些地方的股价贵。

As with price to book, the cheapest countries in the world lie in some of the riskiest parts of the world, in Africa and Eastern Europe. China remains among the most expensive countries in the world but Argentina which also made the list, on a price to book basis, drops back to the pack.

跟市净率一样,股价最便宜的地区在非洲和东欧,这也是是全世界风险最高的地区。在EV/EBITDA比率的基准之上,中国仍然位居全球股价最高的国家之列,不过阿根廷就落到了普通水平。

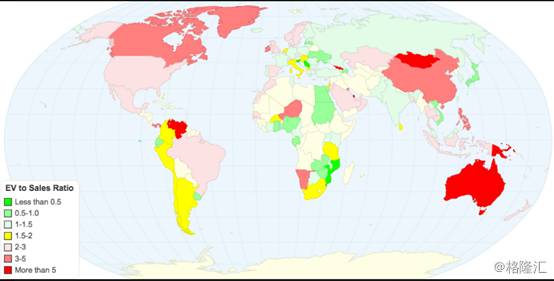

EV to Sales

EV/营收比率

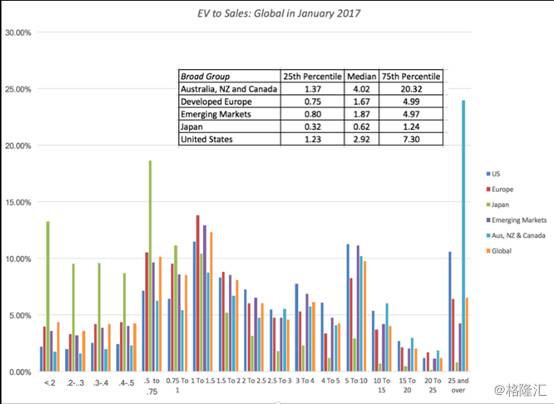

If you share my fear of accounting game playing, you probably also feel more comfortable working with revenues, the number on which accountants have the fewest degrees of freedom. Let’s start with the histogram for global stocks:

如果你跟我一样也担心会计的操控,那你应该会对营收这个数字更放心,因为会计在这个数字上能动的手脚是最小的。我们先来看看全球股票的柱状图:

Of all the multiples, this should be the one where you lose the least companies (though many financial service companies don’t report conventional revenues) and the one that you can use even on young companies that are working their way through the early stages of the life cycle. The median EV/Sales ratio for each country are in the heat map below:

(虽然很多金融服务公司不披露传统的营收),但在所有比率之中,这一项大概是最不可能漏掉公司的一个,即便是处于成长初期的年轻的公司也是能用这个比率的。EV/营收比率的中位数国家热量分布图如下:

By now, the familiar pattern reasserts itself, with East European and African companies looking cheap and China looking expensive. With revenue multiples, Canada and Australia also enter the overvalued list, perhaps because of the preponderance of natural resource companies in these countries.

之前出现过的分布走势又出现了,东欧和非洲的公司看上去依旧便宜,中国的还是很贵。从营收比率来看,加拿大和澳大利亚的公司也进入了被高估的行列,大概是因为这些地域有大量的自然能源公司。

Pricing – Sector Differences

定价-行业差异

All of the multiples that I talked about in the last section can also be computed at the industry level and it is worth doing so, partly to gain perspective on what comprises cheap and expensive in each grouping and partly to look for under and over priced groupings.

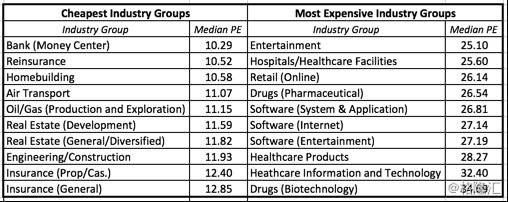

The following table, lists the ten lowest-priced and highest priced industry groups at the start of 2017, based upon trailing PE:

上个部分谈到的所有比率也可以在行业水平上进行计算,而且这样做是很有价值的,一来我们可以看看一个行业里有哪些是便宜的哪些是贵的,二来也便于搜寻低估和高估的行业。下面这张表基于既往P/E列出了2017年初股价最低的十个行业以及股价最高的十个行业。

In many of the cheapest sectors, the reasonsfor the low pricing are fundamental: low growth, high risk and aninability to generate high returns on equity or margins. Similarly, the highestPE sectors also tend to be in higher growth, high return on equity businesses.I will leave the judgment to you whether any fit the definition of a cheapcompany.

在股价最便宜的行业里,低价的原因在于基本面:增长慢,风险高,股权回报率低,利润率低。对应的,拥有最高P/E的行业其增速往往更快,也拥有更高的股权回报。这其中哪些符合你对便宜公司的定义还需要自行判断。

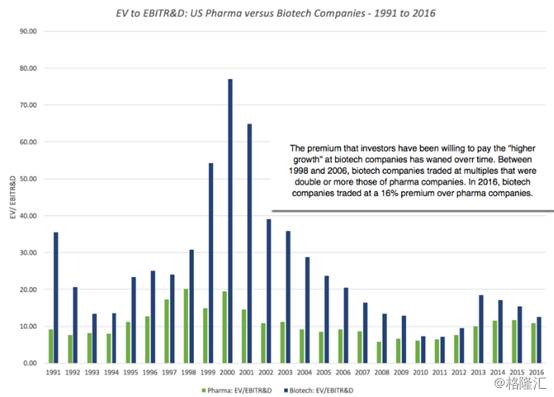

One comparison that you may consider making isto pick any multiple and trace how it has changed over time for an industrygroup. Isolating pharmaceutical and biotechnology companies in the UnitedStates, for instance, here is what I find when it comes to EV to EBITR&Dfor the two groups over time:

你可以考虑任选一个比率,追踪该比率在某个行业里会如何随时间变化。比如,单单拎出美国的制药和生物科技公司,这两个行业的EV/EBITR&D历年变化如下:

You can read this graph in one of two ways. If you are a firm believer in mean reversion, you would load up on biotech stocks and hope that they revert back to their pre-2006 premiums, but I think you would be on dangerous ground.

The declining premium is just as much a function of a changing health care business (with less pricing power for drug companies), increasing scale at biotech companies and more competition.

有两种方法分析此图。如果你十分坚定地相信均值回归,那么你会大量持有生物科技公司,期待这个行业会回复到2006年前的峰值水平,但是我觉得这样做很危险。下降趋势出现主要是因为医疗服务行业在发生变化(制药公司的定价能力被削弱),生物技术公司的规模在扩大,竞争也越来越大。

Rules for the Road

1. Absolute rules of thumb are dangerous (and lazy):

1.绝对的经验法则是危险(且懒惰)的:

The investing world is full of rules of thumb for finding bargains. Companies that trade at less than book value are cheap, as are companies that trade at less than six times EBITDA or have PEG ratios less than one. Many of these rules have their roots in a different age, when data was difficult to access and there were no ready tools for analyzing them, other than abacuses and ledger sheets.In Ben Graham's day, the very fact that you had collected the data to run his "cheap stock" screens was your competitive advantage. In today's market, where you can download the entire market with the click of a button and tailor your Excel spreadsheet to compute and screen, it strikes me as odd that screens still remain based on absolute values.

If you want to find cheap companies based upon EV to EBITDA, why not just compute the number for every company (as I have in my histogram) and then use the first quartile as your cut off for cheap. By my calculations, a company with an EV/EBITDA of 7.70 would be cheap in the United States but you would need an EV to EBITDA less than 4.67 to be cheap in Japan, at least in January 2017.

投资这行里多的是寻找便宜股票的经验法则。比如:交易价格低于账面价值的公司就是便宜的,或者只有6倍EBITDA的公司才是被低估的,再或者PEG(市盈增长率)低于一的公司才是被低估的。在过去,这些法则是站得住脚的,但这是因为那时候数据难以获取,除了算盘、账本就没有别的现成工具研究公司了。在本·格雷厄姆那个年代,会收集数据让他的“便宜股票”筛选器动起来就已经足够有竞争优势了。

在现在的市场里,你只需要点击一下就可以下载整个市场的数据,就可以做一张Excel表格计算然后进行筛选,但让我感到很奇怪的是现在的筛选仍旧是基于绝对价值。

如果你想要根据EV/EBITDA比率找到便宜的公司,那为何不直接计算出每家公司的EV/EBITDA(想我在文中的柱状图中做的一样),然后把前面的四分之一选出来做便宜的公司呢。据我计算,在美国,一家公司的EV/EBITDA达到7.7就算股价便宜了,但是在日本这个数字得到4.67,至少这个情况在2017年1月来看是如此。

2. Most stocks that look cheap deserve to be cheap:

If your investment strategy is buying stocks that trade at low multiples of earnings and book value and waiting for them to recover, you are playing a game of mean reversion. It may work for you, but there is little that you are bringing to the investing table, and there is little that I would expect you to take away. If you want to price a stock, you have to bring in not just how cheap it is but also look at measures of value that may explain why the stock is cheap.

2,很多看上去便宜的股票都是便宜得有理由的:

如果你的投资策略是买入市盈率和市净率低的股票然后等它们回涨,那么你用的是均值回归的玩法。这对你来说可能管用,但是你带上投资桌面上的赌注不多,那我觉得你能够获得的回报也不多。如果你想给一只股票定价,你要弄清楚的不仅仅是这支股票有多便宜,还要看看其价值的计算方式,解释清楚为什么这支股票是便宜的。

3. If you are paying a price, you are "estimating" the future:

When I do an intrinsic valuation (as I did a couple of weeks ago with Snap), I am often taken to task by some readers for playing God, i.e., forecasting revenue growth, margins and risk for a company with a very uncertain future. I accept that critique but I don't see an alternative.

If your view is that using a multiple lets you evade this responsibility, it is because you have chosen not to look under the hood, If you pay 50 times revenues for a company, which is what you might be with Snap, you are making assumptions about revenue growth and margins, whether you like it or not.

The only difference between us seems to be that I am being explicit about my assumptions, whereas your assumptions are implicit. In fact, they may be so implicit that you don't even know what they are, a decidedly dangerous place to be in investing.

3,如果你在给股票定价,那么你其实在“预测”未来:

在预测企业的内在价值时(像几周前给Snap估值时),我经常会被很多读者说成“神算子”,比方说:为未来不明朗的公司预测营收增长、利润率,评估风险。我接受这种批评,但我也别无选择。你认为用比率可以避免这种负担,这只是因为你选择掩耳盗铃罢了。

如果你给以50倍营收买了一家公司的股票,比方说像Snap这样的公司,你其实已经在预测营收增长和净利润率了,无论你喜欢与否。我们之间唯一的区别在于我的假设很鲜明,而你的假设却模棱两可。实际上,你的假设也许已经模糊到你根本不知道自己究竟在假设什么,这种境地对于投资而言是致命的。

·END·