In a milieu of heightened new banking regulations, Hong Kong’s risk premium is plunging to its historic lows that have foreshadowed previous crises. But China’s risk premium remains calm around its long-term average. It is odd. With the new regulations bringing risks previously hidden back onto banks’ balance sheets, banks’ funding costs must rise, and the entire economy will feel it. As such, risk premium must be re-priced higher. But neither the on nor off-shore China market seems to be considering the latent risks. In the past, falsely depressed risk premium distorted the cost of capital in China, keeping Chinese asset valuation higher than it should be, and inducing asset bubbles one after another.

Our trend timing model is still suggesting allocation value for Hong Kong stocks, and has been so ever since February 2016. This model conclusion, together with our elevated but not extreme market sentiment model, paint a more benign market outlook for Hong Kong than the extreme risk premium suggests. With southbound flows increasing through the connect program, the mainland money with higher risk tolerance has moved south, and then depressed the risk premium in Hong Kong. Much to our chagrin, we cannot comprehensively validate this hypothesis with data.

China’s credit growth is slowing, property cycle is peaking and the momentum in its economic recovery is waning. In the US, long-term investment return is locked in a secular decline, albeit experiencing a cyclical rebound since early 2016. Together, they suggest a volatile trading environment for commodities that will test traders’ skills. With rising funding costs, both bond and stock markets are starting to pay for quality. Credit spread is widening, and large caps are outperforming smaller caps. A-shares will remain weak. After consolidation at its current overbought levels, Hong Kong will probably make a final dash towards new high – till the systematic risk suggested by the historic low risk premium unravels.

----------

Diverging Risk Premium between Shanghai and Hong Kong

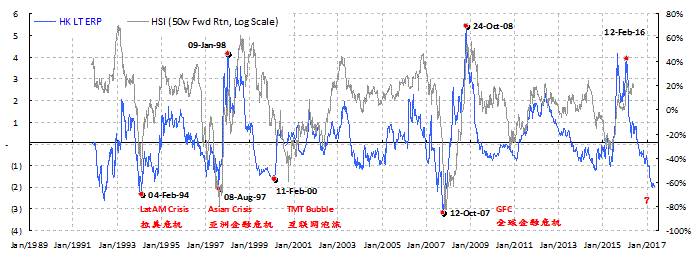

Focus Chart 1: HK risk premium approaching extreme lows consistent with previous crises

Hong Kong market risk premium approaching historic lows, hinting at euphoric sentiment. As Hong Kong surges, its market implied risk premium is plunging towards its historic lows, hinting at extreme market optimism. Historically, when Hong Kong’s risk premium was at its current level or lower, market sank into crises, such as the ‘94 LatAM Crisis, ’97 Asian Crisis, ’00 TMT bubble and finally the ’07 Global Financial Crisis (Focus Chart 1). The current market euphoria is a concern for contrarians. But we have seen other ominous charts recently, such as the chart of an extremely low VIX, and the chart of equal-weighted market indices failing to rise further with the other cap-weighted indices. We must investigate further before drawing conclusion.

Shanghai market risk premium is around its long-term average, even though tightening banking regulation could trigger risk events. Recently, China’s banking regulation tightening is up several notches. In essence, the myriads of new banking rules are trying to make banks account for their credit risks properly. In the past few years, banks have been moving risks off balance sheet to avoid regulatory supervision and risk provision. Consequently, banks, especially the medium and smaller ones, have been able to expand their balance sheets rapidly.

As off-balance-sheet risks are now brought back gradually, banks’ risk provision and funding cost must rise. Previously, these off-balance-sheet risks were hidden and unaccounted for. Risk premium has been suppressed, and consequently the capital cost in the Chinese economy. Chinese asset valuation must have been more expensive than it should be. Now, with the tighter banking regulations, this distorted scheme of risk pricing should normalize.

Focus Chart 2: Shanghai risk premium is around its long-term average, diverging from HK.

The process of revaluing risks in the mainland market will be gradual. “Resolving risks in the existing scheme should not trigger new systematic risk”, as emphasized by the regulators. Together with some intervention from the national team, this is the reason why Shanghai’s market risk premium is lingering around its long-term average, despite a hostile backdrop (Focus Chart 2). As such, the mainland money, which used to be accustomed to a much lower risk premium, buys into Hong Kong through the Connect Program. Such buying with lower risk premium must have depressed the risk premium in Hong Kong, rendering a facade of extreme optimism for now. This is one way to explain Hong Kong’s unusually low risk premium.

The Quality Premium

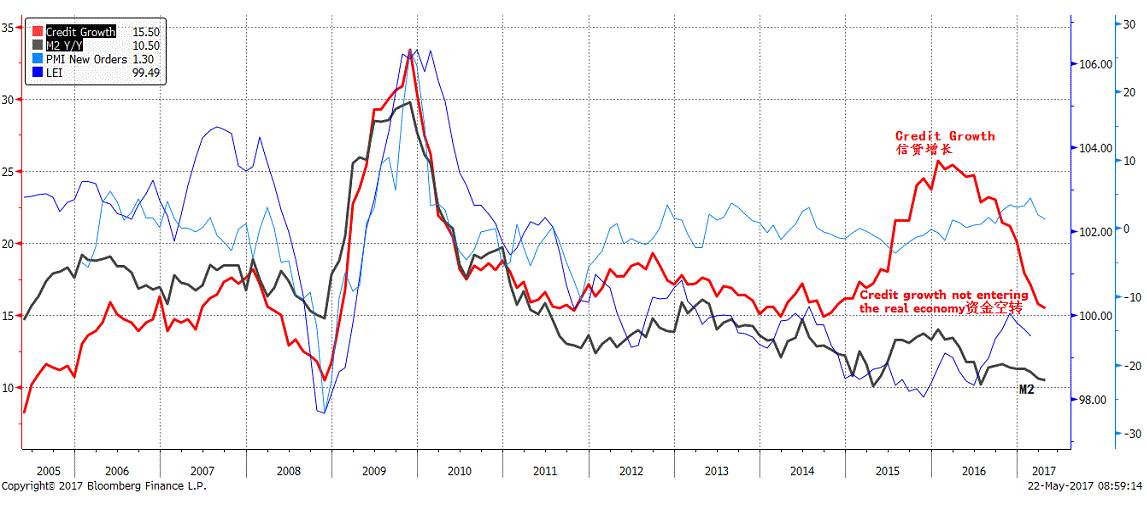

Credit growing on empty. Since mid 2011, around the time of the European sovereign debt crisis, China’s credit growth started to outpace broad money supply growth. The gap between credit and money supply growth had been aggravated further since 2015. It peaked in early 2016, as many market participants were lamenting the “Void of Yield”. This gap is an indication that towards the end, much of the credit growth has not been applied to the real economy. With hindsight, the “Void of Yield” was indeed a surplus of debt. The tightening of credit, as it has been since 2016, tends to bode ill for growth (Focus Chart 3).

With the accounting sleight of hand, it is not difficult to extend credit without expanding a bank’s core liabilities that requires capital provision. A popular practice has been that companies would borrow money or sell bonds and leverage up to buy bank WMPs. This money would then circle back onto the bank’s balance sheet as non-core liabilities, instead of deposits, despite the fact that the transaction is indeed a loan. Consequently, credit growth outpaces money supply growth, and is not entering the real economy. Banks’ balance sheet swells, depressing bond yields for most of 2016.

Focus Chart 3: Credit growth has not entered the real economy, outpacing broad money supply growth.

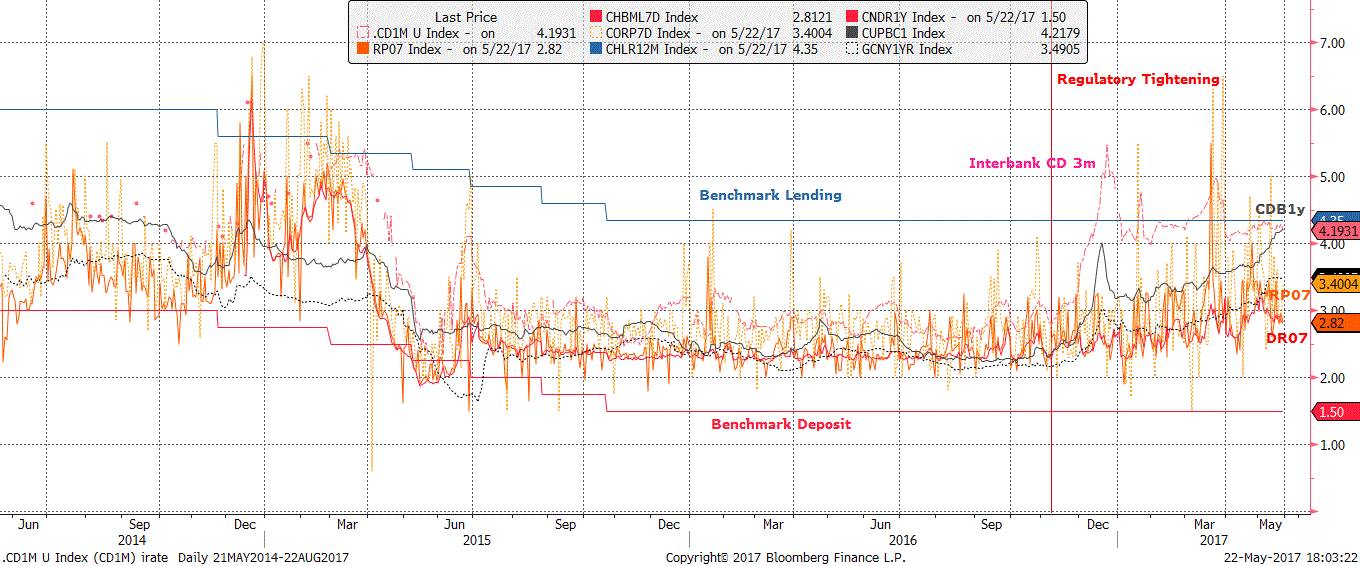

Banks’ funding costs rising. As credit growth slows and off-balance-sheet risk rolls back, banks’ funding costs are rising. For each tranche of banks’ liabilities, from central bank to interbank borrowing, interest rate is higher and more volatile (Focus Chart 4). These changes in funding costs are most palpable in the interest rate of interbank CDs, which at times would surge above the benchmark lending rate. Meanwhile, on banks’ asset side, bond yields are rising and approaching the benchmark lending rate, lowering banks’ appetite to make loans. These changes in banks’ funding costs will eventually permeate to the rest of the economy. Higher financing costs for companies, for example, will be one of the consequences.

Focus Chart 4: Banks’ funding costs rising; the economy will soon feel it.

The market has started to differentiate quality of companies. We note that credit spread between lower-grade bonds and treasury has surged. That is, the credit market is starting to demand a much higher premium on companies with lower credit ratings. The credit spread historically has been highly correlated with the relative performance of large versus small caps, both in China and in Hong Kong (Focus Chart 5). Intuitively, as the financing costs of lower-quality companies start to surge when treasury yields are rising and credit spread is widening, the return on their stocks will suffer. When the market is bullish and is flushed with money, this may not be a hindrance to small caps. But in a bear market as it is now, bond and stock prices should start to reflect the quality difference between companies more closely.

Focus Chart 5: Market starts to pay for quality.

See report “The Year of Rooster: A Trend Breaker” on January 26, 2017

Hong Kong’s Value for Allocation; US Economy Cyclical Recovery

Hong Kong still has allocation value. Despite an ominous prognosis from the extremely low risk premium in the Hong Kong market, our trend timing model is still constructive for the Hong Kong market (Focus Chart 6). So is our market sentiment model. These models have good track records, and have helped us negotiate the market torrents during the “Liquidity Crisis” of June 2013, and the burst of the Chinese bubble in June 2015.

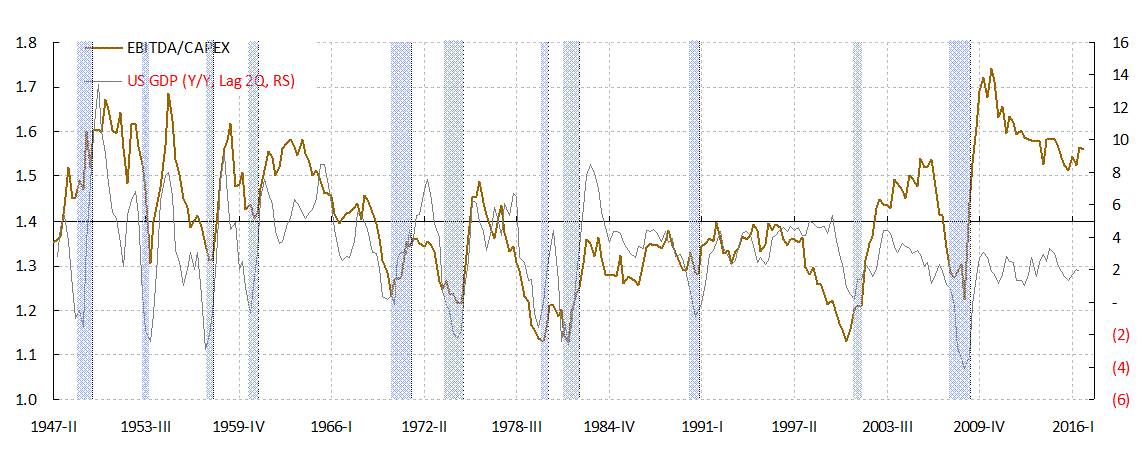

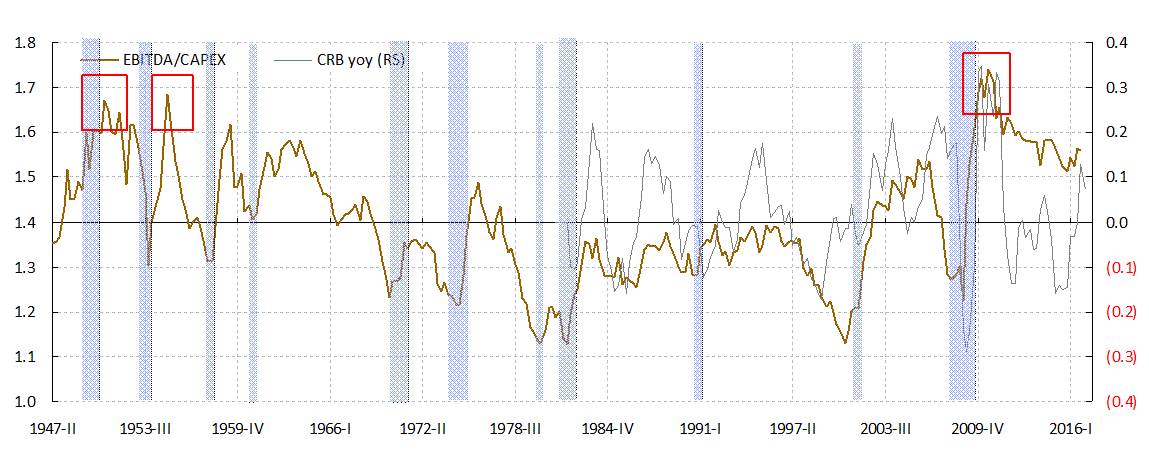

Focus Chart 6: HK still has allocation value, but getting expensive.

Meanwhile, our leading economic indicator for the US, as measured by investment return, is showing the US cyclical recovery is resilient within a secular decline (Focus Chart 7). This indicator leads the US economic growth by two quarters consistently, and correlates closely with the performance of global commodities. If history is a guide, the US economy should perform well in the second quarter. And commodities will remain volatile, offering trading opportunities that will leave traders agonized and frustrated.

Focus Chart 7: The US economy is recovering well.

Hao Hong, CFA

2017-05-24