概要

- 是资本的边际效率相对于利率的突然崩溃,而不仅仅是利率上升导致市场危机。中国资本的边际效率必须进一步提高,才能使每年名义GDP的增量能够维持其宏观形式上的利率负担。中国去杠杆和加强金融监管使市场利率水平和波动普遍上扬。然而,尽管供给侧改革取得了成功,但资本效率改善的速度却落后于利率水平的飙升。

美国10年期国债收益率已飙穿其三十多年的下跌通道。历史上,这种现象往往预示着市场危机。在本轮全球股市暴跌之前,低波动性、高估值和全球央行的紧缩对于市场来说,是一个最糟糕的组合。通过做空市场波动性的交易,或通过市场稳定机制来抑制市场波动性,其实就像是一次拙劣的整容手术——金玉其外,败絮其中。

尽管市场暴跌,但市场情绪仍维持在亢奋水平,显示抛压仍存。价格的暴跌可能会影响目前对经济基本面乐观的看法。通过反身性,市场价格本身就是最根本的经济基础面。短期内,随着通胀压力上升,市场利率仍处于历史低位,即使抛售最后演变成市场危机,全球央行或许也只能是爱莫能助。目前,短期技术面疲弱或可带来技术性反弹。但我们将抗拒这种尝试接飞刀的英雄感。同时,市场可能已经见到了2018年上半年的顶部。

Summary

- It is the collapse of marginal capital efficiency versus interest rate, rather than rising interest rate alone that tends to trigger a market crisis. China’s marginal capital efficiency must improve further, before its incremental nominal GDP can sustain its pro-forma interest rate burden annually. The deleveraging campaign and tightening regulation have triggered a general increase in market interest rates and interest volatility. But the improvement in capital efficiency is falling behind, despite the successful supply-side reform.

In the US, 10-year yield has surged above its long-term declining channel, to a level that portended market crises in the past. Prior to the global sell-off, the combination of low volatility, high valuation and tightening global central banks is the worst recipe for the market. Suppressed volatility, through either vol-shorting trades or through market stabilizing schemes, is like a botched face job – it looks good only on the outside.

Despite the significant market sell-off, market sentiment stays elevated, suggesting selling pressure can be far from concluding. As price plunges, it can affect the current perception of strong economic fundamentals. Through reflexivity, price itself is the quintessential economic fundamental. As inflation pressure mounts in the near term, and interest rates are still at historical lows, central banks’ hands are tied, even if the sell-off spirals into crisis. For now, we would resist the temptation of catching a rebound through short-term technical weakness. And the market may have seen its high for the first half of 2018.

------------------------------

We thank you for your support all these years. In particular, we thank you for voting us as the Best Strategist and the Best Economist, in total 12 top-three awards, in the 2017 "Asia Money" Institutional Survey. We wish you and your family a Prosperous New Year!

这是今天报告的英文原版《

Markets in Crisis

》,感谢阅读。中文翻译版将稍后发出。视频是2018年2月6日盘前与CNBC对市场看法的专访。请点击本文最下方的“

阅读原文

”观看完整视频。

“

But I suggest that a more typical, and often the predominant, explanation of the crisis is, not primarily a rise in the rate of interest, but a sudden collapse in the marginal efficiency of capital.

The later stages of the boom are characterized by optimistic expectations as to the future yield of capital-goods sufficiently strong to offset their growing abundance and their rising costs of production and, probably, a rise in the rate of interest also.

It is of the nature of organized investment markets, under the influence of purchasers largely ignorant of what they are buying and of speculators who are more concerned with forecasting the next shift of market sentiment than with a reasonable estimate of the future yield of capital-assets, that,

when disillusion falls upon an over-optimistic and overbought market, it should fall with sudden and even catastrophic force.

Moreover, the dismay and uncertainty as to the future which accompanies a collapse in the marginal efficiency of capital naturally precipitates a sharp increase in liquidity-preference – and hence a rise in the rate of interest.”

–

General Theory of Employment, Interest and Money, John Maynard Keynes

Markets in Crisis

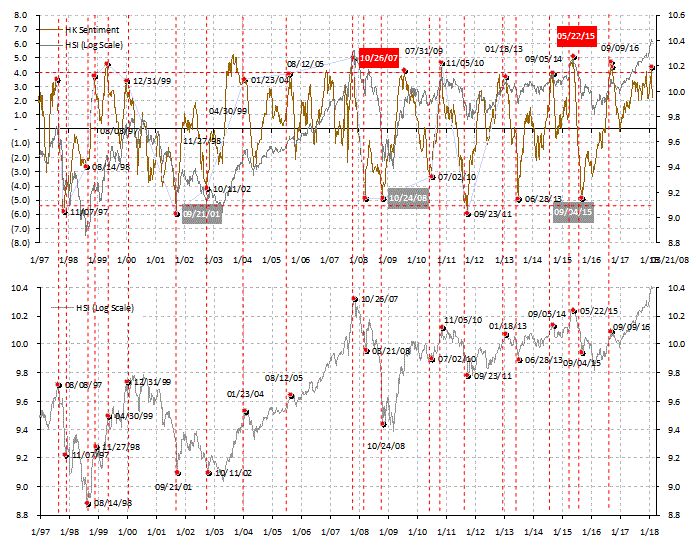

Market sentiment remains elevated despite a significant sell-off.

As we write, global markets continue their epic sell-off. Despite the plunge, market sentiment remains elevated. Of course, as the global markets roil, our market sentiment index will continue to shift towards a more neutral stance. But with market sentiment at its elevated level currently, the selling pressure does not appear to be concluding any time soon (

Exhibit 1

). As such, we would not attempt to catch falling knives, or be lured into technical rebounds that tend to follow any significant correction, before the dusts settle.

In our most recent report titled “

The Year of the Dog: Lessons from 2017

”, just three trading days before this plunge, we warned of an impending correction.

We suggest that we need to wait for the near-term market excess to dissipate, before re-establishing our market positions.

Our sentiment indicator, albeit not infallible, has an excellent track record. For instance, it pinpointed the market peak in October 2007 when the Shanghai Composite was above 6000 points, and again in June 2015 when the Composite was above 5000 points - two of the biggest stock market bubbles in recent history.

During market crisis, the correlation between markets quickly approaches one. As such, our sentiment indicator is a snapshot of global market conditions, especially at inflection points.

Exhibit 1: Market sentiment has declined from extreme, but remains elevated.

Surging interest rates due to China’s deleverage campaign portends market risks.

In our 2018 outlook report titled “

View from the Peak

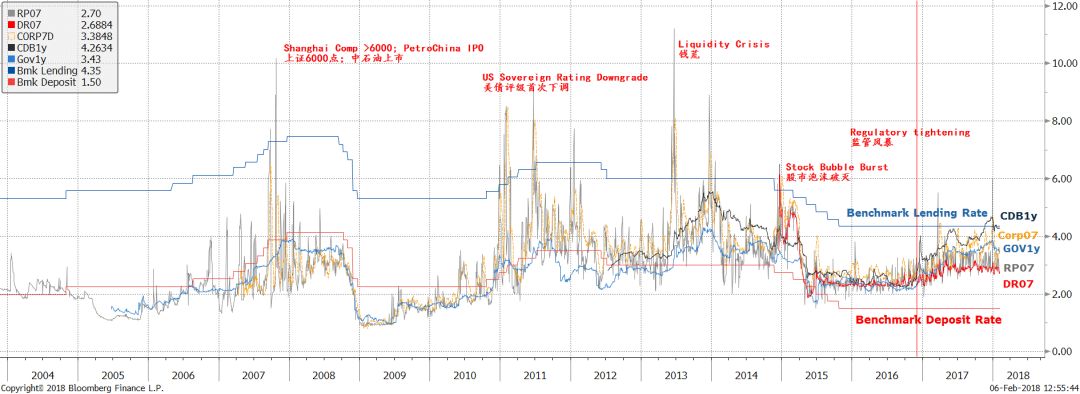

” on 4 December 2017, we discussed how China’s deleveraging campaign had triggered a general rise in market interest rates in the domestic Chinese bond market. Indeed, the sell-off of bonds in November and December at times has been epic. And for the first time in history, the CDB one-year yield surged above the one-year benchmark lending rate.

Such occurrences tended to herald market crises in the past, as we wrote in our 2018 outlook report (

Exhibit 2

).

In the same 2018 outlook report “

View from the Peak

”, we foresaw an investment style change sometime during the first quarter, and posited that the market would look very different before and after the first quarter.

Exhibit 2: Surging Chinese bond yields above benchmark lending rate portended market crisis in the past.