概要

全球经济周期筑底修复。

2019年确实是“峰回路转”的一年 - 与2018年底时普遍的悲观情绪相反。

现在,我们的中国经济周期领先指标正在见顶,并很可能在未来几个月开始放缓。

考虑到中国经济周期指标的领先性,假设贸易谈判能取得一定的进展,中国经济的名义变量(如工业增加值和公司盈利增速等)应该会开始修复。

在中国经济周期指标率先回升之后,欧美的经济周期也正在筑底。

尽管如此,这些都是同步或滞后的经济变化。

2018年的抛售潮后,市场已经显著反弹。

因此,市场价格在2019年的涨势很可能已经反映了这些滞后经济变量现在的回暖 - 除非今后基本面的改善大幅超预期,从而进一步大幅推升股市。

但中国的超级猪周期使短期通胀前景恶化。

猪瘟摧毁的中国生猪存栏量几乎相当于整个欧盟的猪存栏。

中国生猪存栏量的变化往往领先猪价上涨约6个月。

因此,通胀压力很可能持续飙升到春节过后,并在短期内限制货币政策的选择。

这种货币政策的困窘很可能会阻碍股市短期上行的动能和空间。

在未来的12个月内,上证综指的交易区间底部很可能约为2,700,而上证850天移动均线始终不能突破自2010年以来3200点的顶部。

即使指数的现价或可暂时突破该水平,这个长期移动平均线的潜在趋势还是在下降的。

我们的股债收益率模型的交易区间实际预测分布是2,500-3,500。

除非引入外来因素,例如国外流动性的大量流入,否则中国股市将仍然是一场零和博弈。

尽管市场整体机会有限,“龙头效应”仍将持续。

过去十年,中美行业集中度都越来越高,行业龙头在行业收入中所占的份额越来越大,并且产生更高的股本回报。

尤其是在中国,大盘股的股本回报率高于资金成本,而中小盘股却不然。

鉴于行业内领先地位的变更性非常有限-后来居上的机会只有4%,股票的“龙头效应”将持续存在。

强者恒强,赢者通吃。

因此,尽管整体市场机会有限,沪深300、A50、上证50、离岸大盘中概股等最能反映“龙头效应”的指数应仍能提供投资机会。

全球收益率下降表明,周期性股票、小盘股和新兴市场长期跑输的趋势仍未结束,但有些交易员可能会尝试从近期的超卖反弹中获利。

自2010年以来,中国的股本回报率一直在下降。

与此同时,以美国的EBITDA /资本支出来衡量的全球投资回报亦然。

对于未来的悲观情绪导致全球储蓄过剩,并压抑回报率。

因此,具有获得超额投资回报能力的公司应该享有溢价,如行业龙头。

周期性股票、小盘股和新兴市场长期跑输的趋势与全球投资回报率下降密切相关。

只要全球投资回报率继续下降,这种长期趋势就没有结束。

话虽如此,交易员近期可能会试图交易全球央行重启量化宽松而引发的、这些资产类别的超跌反弹。

美股仍有新高。

但长期趋势重于短期波动。

这是我们20191110的报告《

展望2020:

静水流深

》的英文原版。感谢阅读。

----------------------------------------

Global healing of economic cycle.

2019 truly has been a year of “Turning a Corner” – contrary to the prevailing pessimism at the end of 2018. Now, our leading indicator of China’s economic cycle is peaking, and will likely moderate in the coming months. Given the leading nature of our cycle indicator, assuming some progress on the trade front, nominal economic variables in China, such as IP and earnings growth, will likely begin to recover. The cycle in the US and EU is bottoming out, following China’s lead with a lag. That said, these are coincidental or lagging variables. Their reflation is likely to have been reflected in a market that has rebounded significantly from the 2018 selloff – barring significant upside surprise in fundamentals.

But China’s super hog cycle intensifies inflation outlook.

The swine flu has devastated China’s pig stock by almost the entire pig population in the EU of ~150m. The change in China’s pig stock tends to lead the hog inflation by ~6 months. As such, inflation is likely to surge well past the Chinese New Year, hamper monetary choice in the near term, and retard the momentum and upside in stocks. In the coming 12 months, the Shanghai Composite’s bottom will likely be ~2,700, with 3,200 being the peak level on the 850-day moving average since 2010. The actual forecast of trading range dispersion by our EYBY model is indeed 2,500-3,500. Spot price could temporarily break above this level. But the underlying trend of the moving average is declining. Unless exogenous factors are introduced, such as significant inflow of foreign liquidity, China’s stock market will remain a zero-sum game.

Although broader market offers limited opportunity, the “leader effect” will persist.

Both Chinese and US industries have been increasingly concentrated over the past decade, with industry leaders reaping greater shares of industry revenue and enjoying higher ROE. For China, large caps are earning an ROE > cost of capital, but this is not the case for the small/mid-caps. Given that the mobility to move up to the top ranks within an industry has been very limited – only 4% chance, the “leader effect” in stocks will persist. And indices that best capture this effect, such as CSI300, A50, SSE50, and offshore Chinese large caps, will continue to offer opportunities.

Falling global return suggests the secular underperformance of cyclicals, small caps and EM has not ended, but some may be tempted by near-term oversold rebound.

China’s ROE has been falling since 2010, concurrent with the global investment return measured by US EBITDA/capex. Glooms about the future have created a global savings glut and depressed return. As such, the ability to earn a return above capital costs should command premium, such as China’s industry leaders. The secular underperformance of cyclicals, small caps and EM is highly correlated with falling global return. This secular trend has not ended, so long as global return continues to fall. That said, traders may be tempted by an oversold technical rebound in these assets spurred by global central banks’ re-QE in the near term. The US is heading for new highs. In the long run, however, secular trends trump technical moves.

Going the Distance

China’s Super Hog Cycle in 2018-2020

Since March 2017, we have researched extensively into the well-defined short cycles in the US and Chinese economies. These cycles by themselves are endogenous to the underlying dynamics in the economy. When economic cycles move, they fluctuate with regular cyclicality and simultaneity across a vast array of economic variables, and engender ebbs and flows in the economic trajectory.

Based on our economic cycle theory and quantitative models, from 2H2017 to FY2019, our outlook reports were titled “

Going for New High

” (for 2H2017), “

View

from the Peak

” (for FY2018), “

Rough Sailing

” (for 2H2018) and “

Turning

a Corner

” (for FY2019), respectively. With hindsight, the direction of China’s economy and its markets has been largely consistent with our cyclical models’ forecasts.

In the coming months, China’s leading economic cycle indicator, which has been stabilized by the property investment in 2019, is likely to moderate. The signal of an inflection year from our leading cycle indicator has been reflected in the general recovery of the stock market in 2019. If the trade negotiation can further progress amid the already reconciliatory tones from the US and China, a global recession can be dodged. If so, 2020 will be a year of greater domestic focus, with the US getting on with its presidential election, and China trying to regroup to steady its economy. But the inflation outlook is less certain.

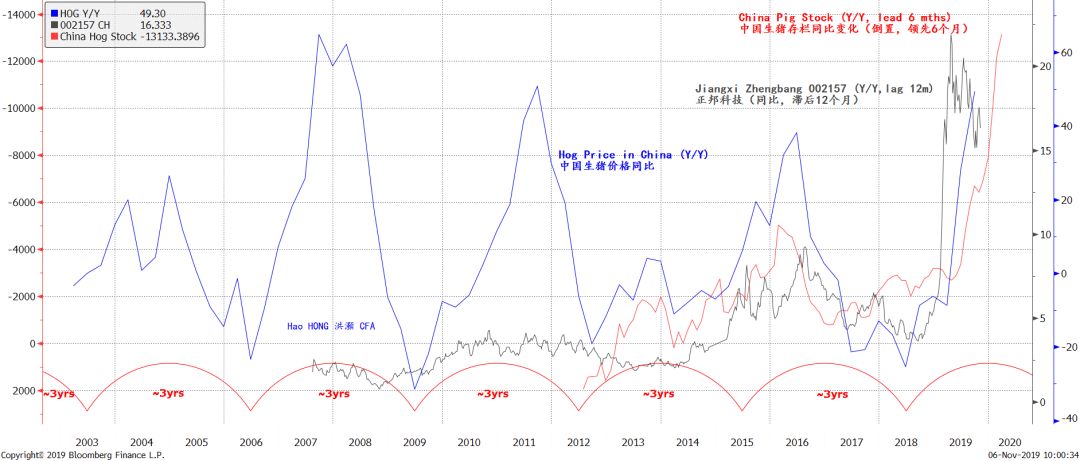

Figure 1: China’s super hog cycle from 2018 to 2020 is unprecedented

Source: Bloomberg, BOCOM Int'l

The shortfall in pig stock tends to lead hog price inflation by about 6 months historically (

Figure 1

). Since the second half of 2018, the pig stock in China has been devastated by the severe outbreak of the African Swine Fever. The country’s pig stock has now fallen by ~130 million year on year, which is close to the entire pig population of ~150 million in the EU, and almost double the size of that of the US.

The intensity of the current hog price inflation in China rivals the previous peaks in history (

Figure 1

). However, the reduction of pig stock in China is unprecedented, and is likely to induce a super hog cycle unseen before. The hog cycle in China tends to run for approximately three years, and its wave length has been largely consistent with that of China’s short economic cycle. Given the severe pig shortage, this hog cycle can run substantially higher than previous cycles. It will hamper the choice of monetary policy in the near term, lessening the chance and the depth of any potential rate cut.

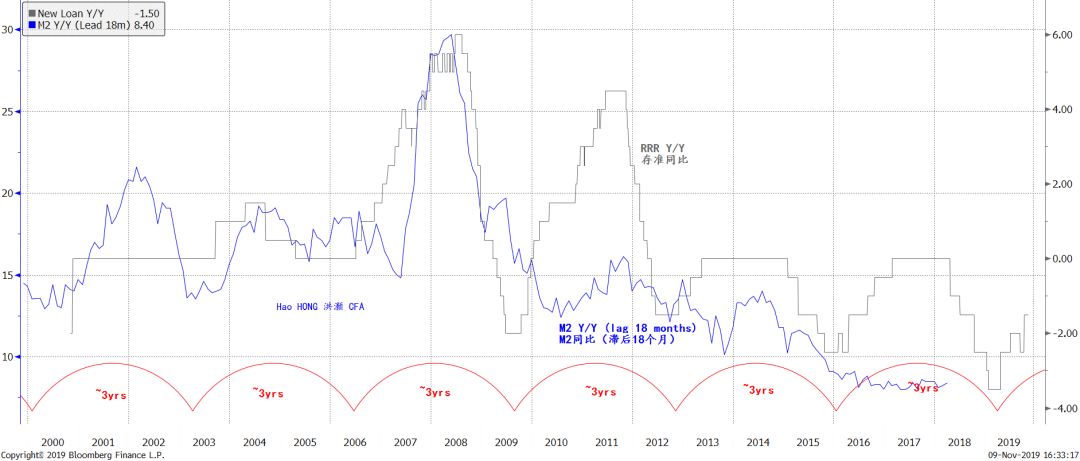

Figure 2: The effect of RRR cuts on monetary condition has a long lag, especially when inflation is high

Source: Bloomberg, BOCOM Int'l

China’s RRR cuts have so far failed to generate sustainable lending growth. This is because RRR cuts tend to influence monetary conditions with a lag of up to 18 months (

Figure 2

). The change in RRR also runs with a cycle of roughly three years. In early 2019, we have seen this long leading indicator bottoming out. As such, easing liquidity conditions will come eventually, although we must wait a little while longer - till the inflation pressure starts to dissipate.

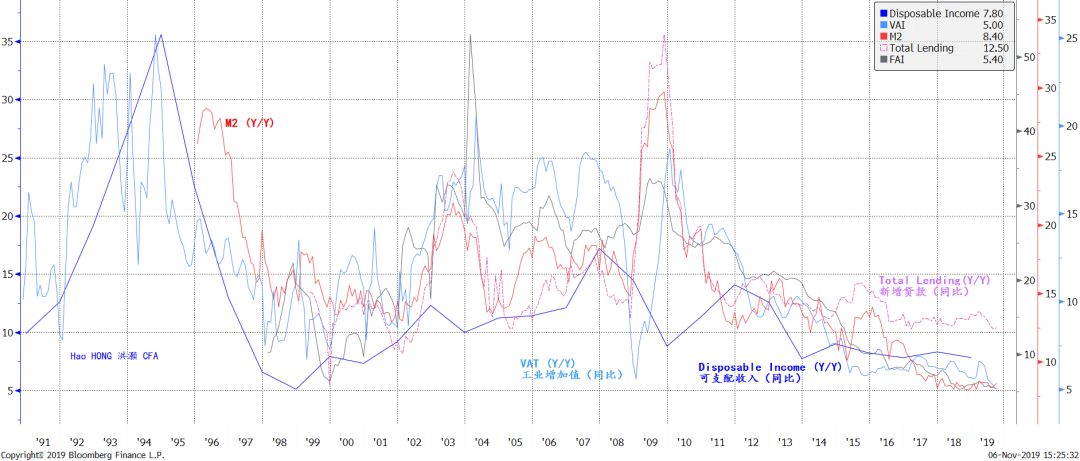

Even though inflation pressure driven by China’s super hog cycle is likely to mount in the coming months, we believe the longer-term trend for inflation is still declining. The PBoC’s monetary objective has remained surprisingly neutral and restrained, with a stated policy objective to keep M2 growth consistent with nominal GDP growth.

Money supply growth determines lending, investment, economic growth, and ultimately the growth of disposable income. If the longer-term trend of M2 growth is falling, so will disposable income growth (

Figure 3

). As such, as long as productivity gain, which is increasingly from the exponential growth of computing power, rises faster than income, as it has been, the longer-term outlook for inflation should be declining as well.

Figure 3: Falling money supply, investment, growth and hence income curtail longer-term inflation

Source: Bloomberg, BOCOM Int'l estimates

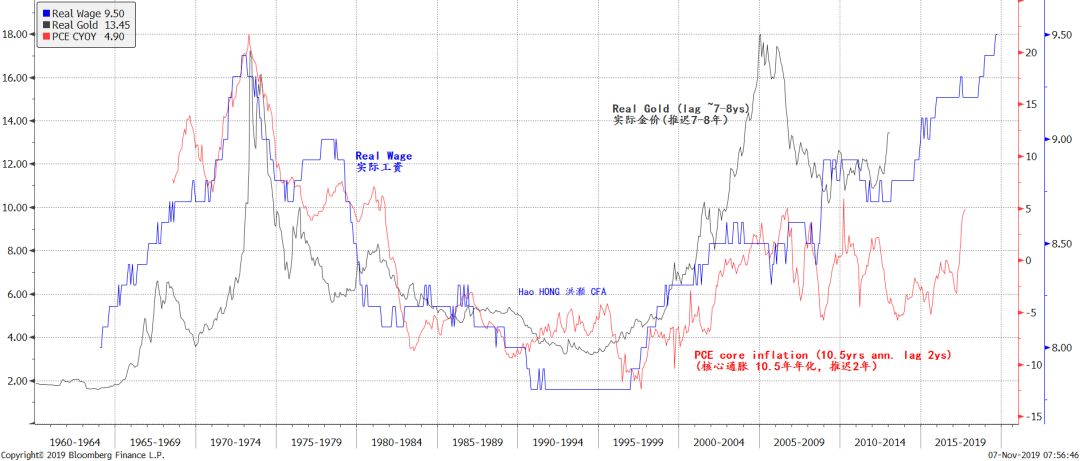

In the US, we find that inflation pressure is slowly building as well. We note that the real wage in the US has returned to its previous highs seen in early 1970s. If we compare the US real wage with US PCE core inflation annualized on a 10.5-year basis with a roughly two-year lag, we can see a clear correlation, and a trend of rising US core inflation (

Figure 4

; Note that the 10.5-year basis for our analysis is consistent with the wave length of an intermediate economic cycle consisting of three 3.5-year short cycles.

There is also close correlation between real wage in the US and the inflation-adjusted gold price, with a lag of roughly seven years (the wave length of an intermediate cycle consisting of two 3.5-year cycles). In short, real wage growth can forecast the direction of US inflation and gold price, with a substantial lead (

Figure 4

).

Figure 4: US core inflation pressure is slowly accumulating, as US employment reaches cycle peak

Source: Bloomberg, BOCOM Int'l estimates

If inflationary pressure in the US is indeed slowly rising, as suggested by

Figure 4

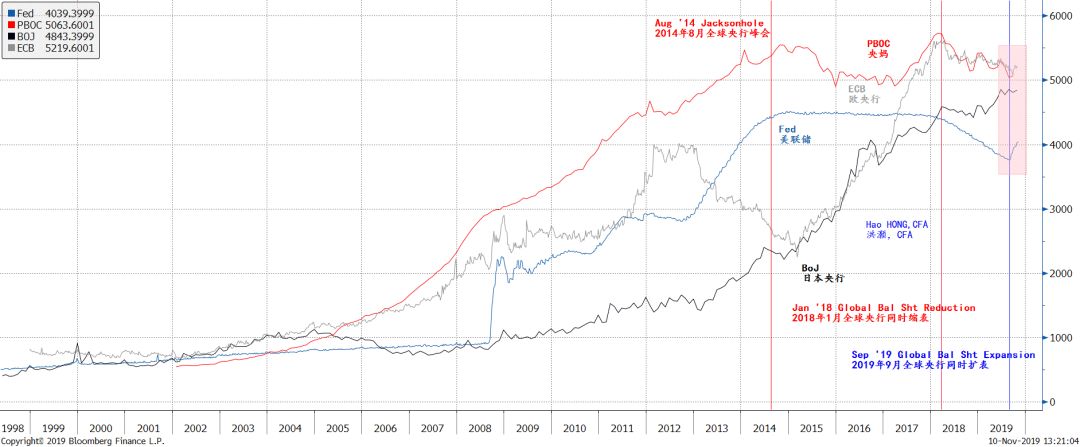

, and the short economic cycle is healing (to be discussed later), the Fed’s path to rate cuts as anticipated by the market could be altered. But the Fed’s plan to re-expand its balance sheet together with the other major global central banks is likely to be intact (

Figure 5

).

Figure 5: Global central banks are re-expanding their balance sheets

Source: Bloomberg, BOCOM Int'l estimates

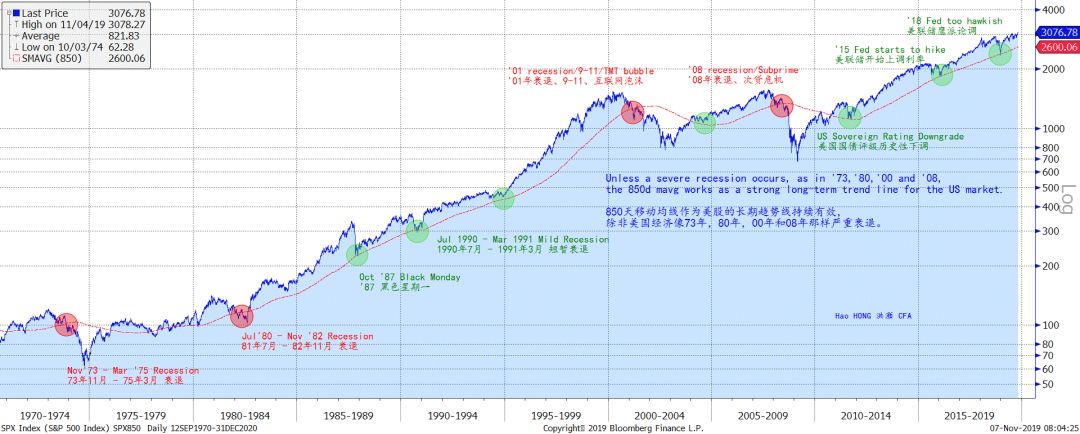

Such a discrepancy in the market’s expectation of rate cuts, though in part being gradually reflected in the Fed funds futures, can induce disruption in the stock market in 2020. That said, without recession, the rising trend in the US market will persist, with the 850-day moving average being the secular rising trend line (

Figure 6

). The last leg up will likely squeeze many doubters of the US market’s strength, burying a lot of shorts and then the longs after the eventual market peak.

Figure 6: 850-day mavg is a secular rising trend line for SPX; only severe US recessions could puncture it

Source: Bloomberg, BOCOM Int'l estimates

China’s Leading Econo

mic Cycle Indicator to Moderate

In our initial report on economic cycles with quantitative metrics titled “

A Definitive Guide to China’s Economic Cycles

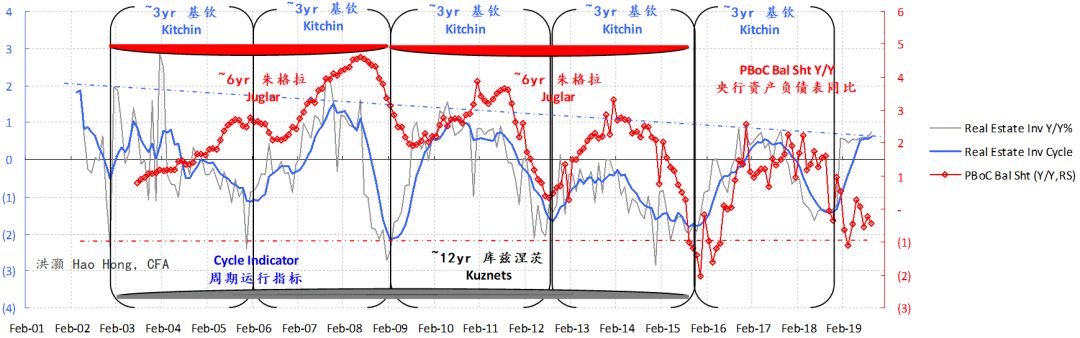

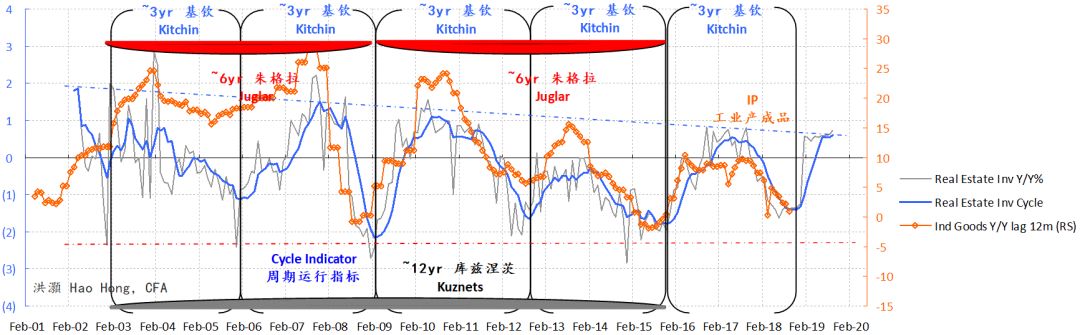

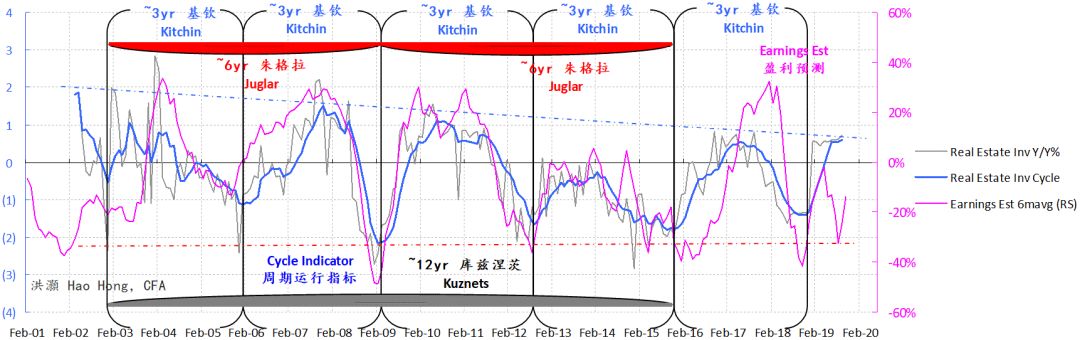

” (20170324), we demonstrated the 3-year short cycle in the Chinese economy. We derive our 3-year investment cycle by measuring the deviation of the actual property investment growth data from its long-term trend. There have been by now almost six, very clearly-defined 3-year cycles in China’s economy: 2003-2006, 2006-2009, 2009-2012, 2012-2015, and the last quarter of 2015/early 2016 till the end of 2018.

To verify the 3-year short cycle, we compare it with other macroeconomic variables in terms of both volume and price in the Chinese economy. Rebar price, interest rate level, industrial output, stock market indices and earnings forecasts, for instance. We have demonstrated that these variables are closely correlated (not all comparisons are shown in this report; for detailed discussions on China’s short economic cycle, please refer to our report “

A Definitive Guide to China’s Economic Cycles

” on 20170324). That is, the 3-year short cycle can very well explain the movements in many other Chinese macroeconomic variables (

Fig

ure 7

).

Further, we note that in the past two decades of which period we have data, the trend of investment growth is falling, with lower highs and lower lows in each of the cycle sequentially. This is not difficult to fathom: China’s massive investment scale and increasing leverage are suppressing marginal investment return, and thus limiting the room for further productive investment.

We believe the duration of the 3-year cycle is related to China’s building construction process. For instance, to build a 30-storey residential building, the building completion time is around 9-12 months, water and electrical installation around 3 months, plus some more time for safety inspection and miscellaneous approvals. The total time to completion is around 1.5-2 years. Then, the building inventory will take up to 1 year to clear, making the building inventory investment cycle of around 3 years.

We note that the current 3-year short cycle that started from late 2018 to early 2019 is peaking, driven by moderating property investment growth after double-digit growth in 2019. That said, as our cycle indicator is a leading measure, the momentum in nominal economic variables driven by surging inflation pressure can still show persistency in the coming months (

Figure 7

).

Investors should not be fooled by these nominal and lagging improvements that have been well foretold by our cycle leading indicator and thus are already priced in. Unless the nominal improvements beat market expectations significantly, stock prices will not respond. In general, in a slowing environment with persistent inflation pressure in the coming months, investors will find it difficult to commit capital to stocks or bonds.

Figure 7: China’s leading economic cycle indicator will likely moderate in the coming months, but China leads

Source: BOCOM Int'l estimates

The Global Cycle is Healing

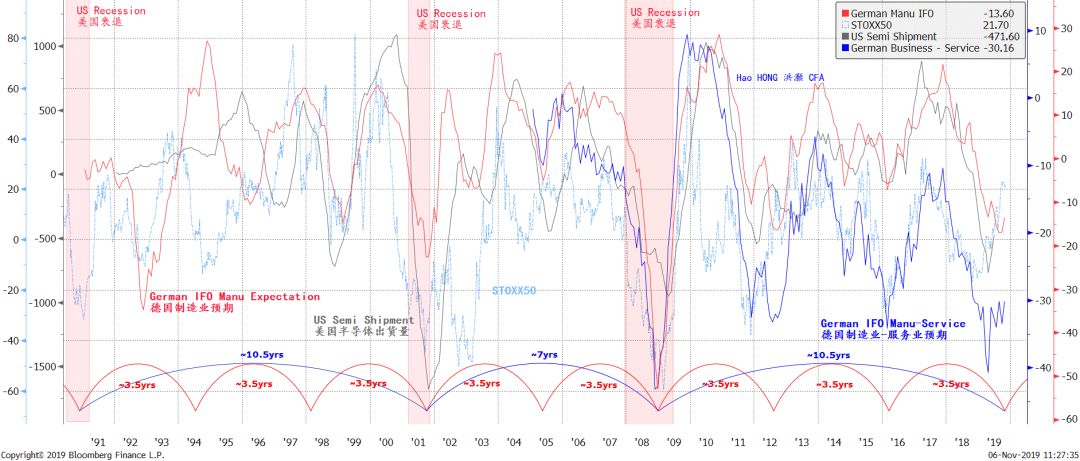

Globally, the short economic cycle appears to be bottoming out in both EU and the US (

Figure 8

). The short economic cycle in the EU and the US, as approximated by German manufacturing IFO, US semi shipment growth and EPS growth, operates with a wave length of roughly 3.5 years (“

The Colliding Cycles of the US and China

” 20180903 and “

A Definitive Guide to Forecasting China Market

” 20190920). Its length is largely consistent with China’s short economic cycle, but runs with a lag.

Figure 8: The short economic cycle in both the EU and the US is healing

Source: Bloomberg, BOCOM Int'l estimates

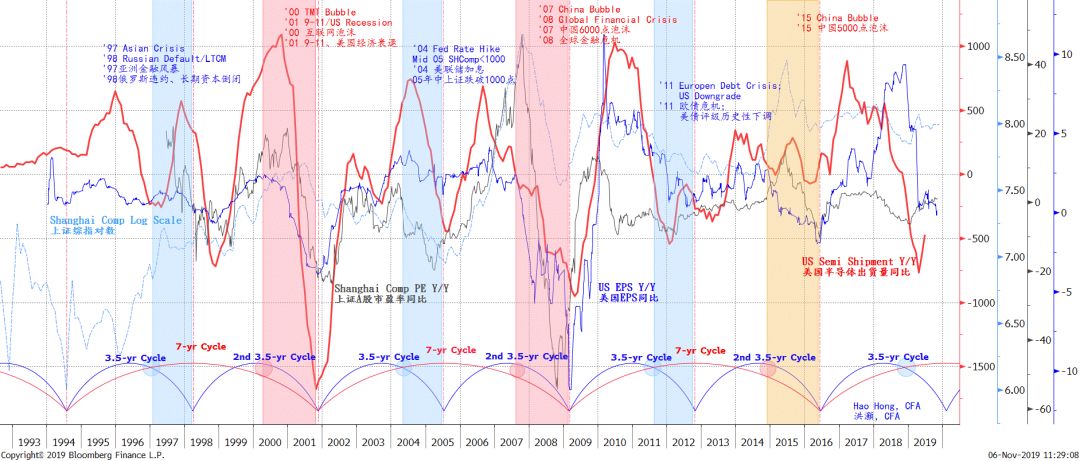

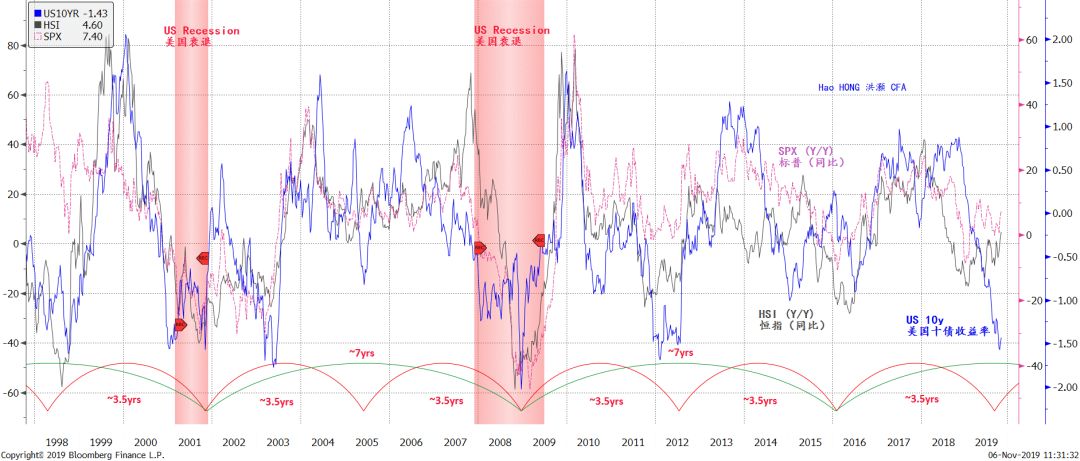

Meanwhile, the US 10-year yield is bottoming out from a very depressed level that historically augured economic recession or market turmoil, as in 2001/02, 2008, 2012 and 2015/16 (

Figure 9

). Yield curve re-steepening can alleviate the recession fears. As China’s cycle of stock market return continues to recover from the bottom of a 7-year cycle seen in late 2018 and early 2019, the US Leading Economic Indicator is reflating concurrently (

Figure 10

). Yet, the market remains skeptical about the health of the US economy, despite the help from the Fed.

Figure 9: The global cycle is healing (cont’d)

Source: Bloomberg, BOCOM Int'l estimates

Figure 10: China’s cycle is leading the global cycle

Source: Bloomberg, BOCOM Int'l estimates

As such, the strength of the US market rebound can surprise many bears – as the final short squeezes prior to the eventual market downturn always do. In 2020, we would also watch the US election closely. It will be a showdown between the capitalists and the socialists. For now, it is difficult to fight the global central banks that are re-expanding their balance sheets simultaneously.

A History of US Investment Return and its Implications

In our previous report titled “

A Definitive Guide to Forecasting China Market

” (20190920), we discussed that 2010 is the watershed year in asset allocation in China. Current account surplus to GDP ratio, money supply growth and FAI growth all peaked around 2010 and have declined ever since then.

Consequently, the 850-day moving average of the Shanghai Composite has not made any new high above ~3,200 since 2010. China’s stock market has turned into a zero-sum game since then. Even the bubble in 2015, though significantly breaking through 3,200, did not take the moving average to new higher levels.

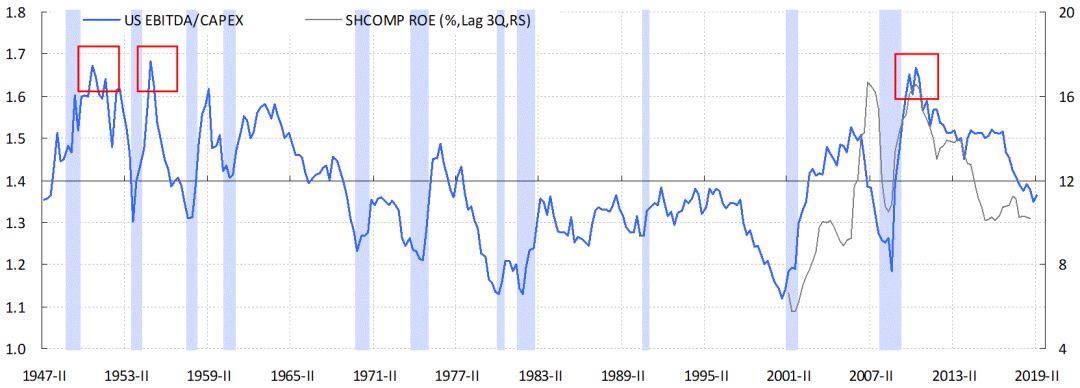

Globally, we notice a similar development. Using the US Flow of Funds data, we calculate the EBITDA-to-Capex ratio in the US economy, and use this ratio as a proxy for investment return in the US. We find that investment return in the US has also peaked around 2010, and has been falling ever since, albeit not to the recessionary levels seen during the recessions since 1970s. As our analysis shows, the ROE of the Shanghai Composite and the US investment return are closely related (

Figure 11

).

Figure 11: US investment return and China’s ROE have both been falling since 2010/11

Source: Bloomberg, BOCOM Int'l estimates

It is difficult to dismiss this correlation as mere coincidence, given the inter-dependence between the US and Chinese economy. Historically, China produces and US consumes. The US spends and China saves. The accumulations of positions for FX purchases, or the PBoC’s sterilization operations, have been the most important source of liquidity for China.

Since the Great Recession in 2008, however, the US has been disenchanted by gloomy outlook and has been saving hard. This change in saving habit can be seen in the rising national savings rate in the US, concurrent with the rising current account surplus. The savings glut depresses investment return, and affects the investment outlook for the US public, who in turn saves even harder. Consequently, investment return in the US continues to fall, as seen in

Figure 11

.

Meanwhile, in China, because the foreign source of liquidity is dwindling, Chinese growth that used to be driven by credits starts to slow, and hence ROE. Indeed, we observe falling ROE across all market caps in China since 2010. And the ROE of mid/small caps is falling much faster than that of large caps, and is now well below the equity discount rate. That is, the mid/small caps are now earning negative economic return, while the large caps are managing to stay above the general equity discount rate (

Figure 12

).

Figure 12: Return in China has been falling; divergence between large and mid/small caps

Source: Bloomberg, BOCOM Int'l estimates

Such diverging ROE between large and mid/small caps explains the “leader effect” in recent years, as the leading companies in their respective industries substantially outperform the rest of the industry. Similar market performance as a result of industry concentration is also seen in the US.

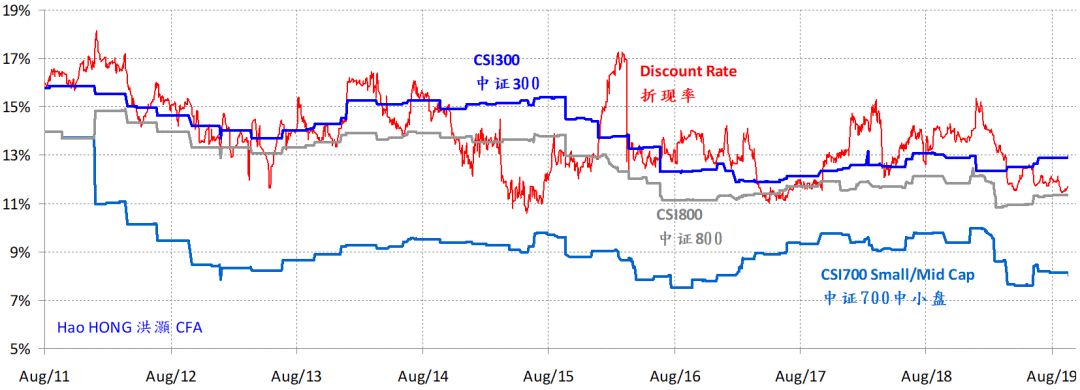

The relationship of the large-cap index with its 850-day moving average contrasts starkly with that of the small/mid-cap index. For the large-cap indices represented by the SSE50 or CSI300, they stay well above the 850-day moving average. The average has been acting as a strong support for the underlying rising trend of the large caps. On the contrary, the moving average is acting as a strong resistance for the small/mid-cap indices represented by CSI700, and the overall broad market index of the Shanghai Composite (

Figure 13

).

As such, without a major paradigm shift for the small/mid-caps, we should expect continuing relative outperformance from the large caps. Even the targeted policies to help out the small businesses may not be able to turn the tables for now.

Figure 13: The 850-day mavg is a strong resistance for the Shanghai Comp, but a strong support for SSE50

Source: Bloomberg, BOCOM Int'l estimates

The US investment return, as measured by the ratio between EBITDA and Capex, is also an excellent proxy for the global investment environment. Our analysis finds the US investment return highly correlated with the relative performance of global cyclicals vs. defensive, EM vs. the world, and small vs. large caps (

Figure 14

).

Since around 2010, cyclicals, EM and small caps have been underperforming. That said, even though by now the underperformance has persisted for years, and may be prone to a technical rebound in the near term, it is unlikely to have run its course. Ever falling interest rates, and the prospect of negative interest rate, will prompt people to save harder, as suggested by the Japanese experience.

And as long as the glut of savings persists, investment return will remain depressed, auguring ill for the relative performance of small caps, EM and cyclicals. One should not mistake a technical rebound in these risk asset classes, however strong, for the ultimate turn of the secular trends that have been persisting since 2010.