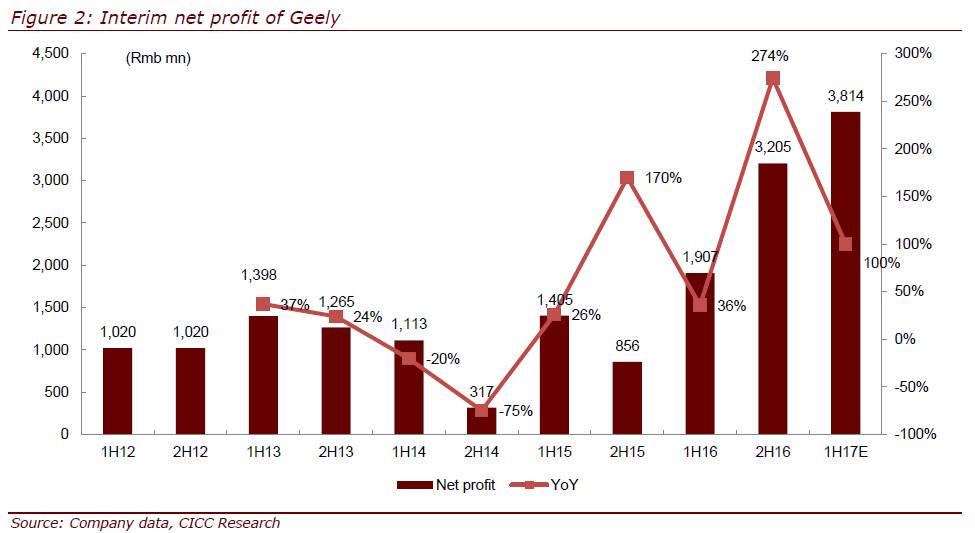

1H17 earnings expected to rise >100%YoY

Geely preannounced its net profit might grow >100% YoY in 1H17, implying >Rmb3.82bn.

Trends to watch

1H17 may beat expectations; profitability per car continues to rise.

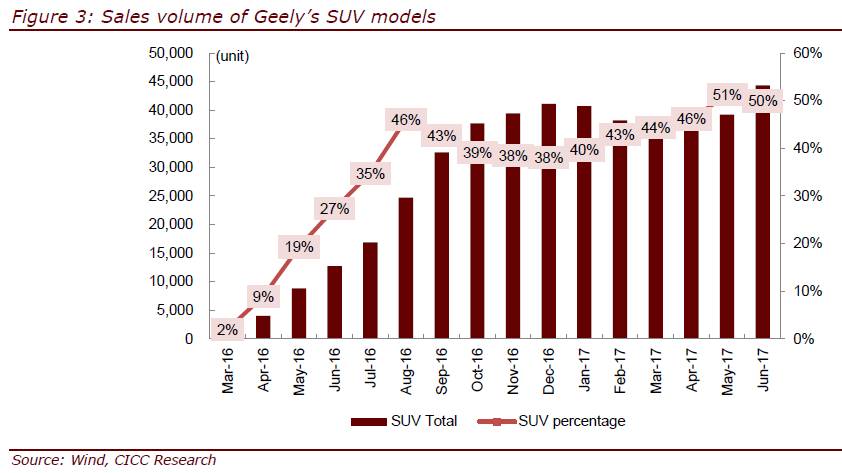

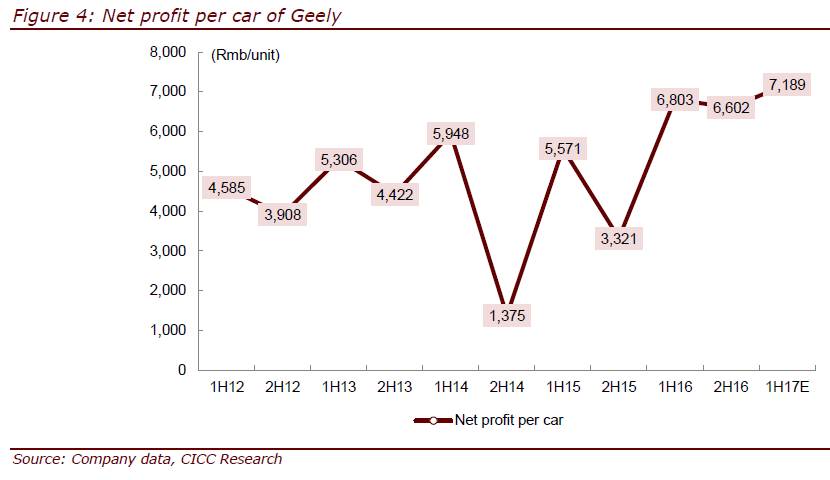

Geely expects its 1H17 earnings to rise >100% YoY & >19% HoH; we attribute this to: 1) we estimate Geely’s Generation 3.0 models’ GPM is +0.5ppt HoH to 19.1% in 1H17; 2) costs should be well controlled, with SG&A cost ratios further reduced 0.5~0.6ppt; and, 3) sales structure continues to be optimized, SUVs contributed 45% in 1H17, and 50% in June. Besides, NP/car +6% YoY & +9% HoH in 1H17, representing higher profitability per car.

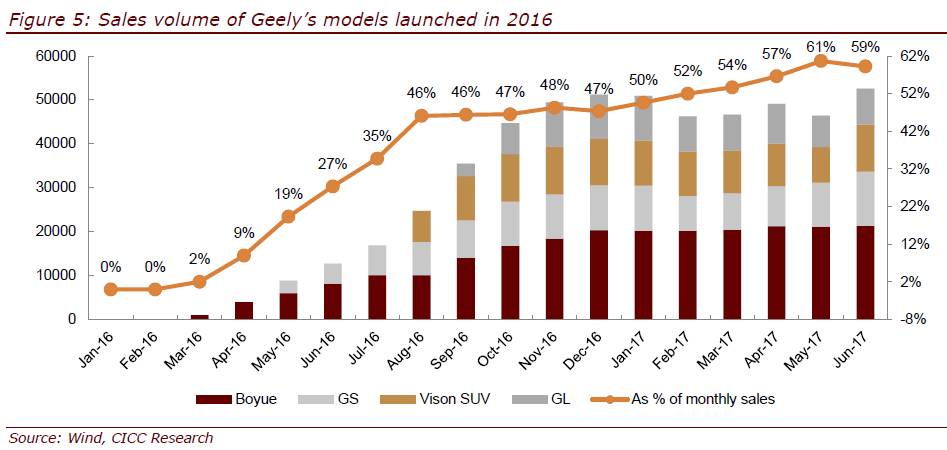

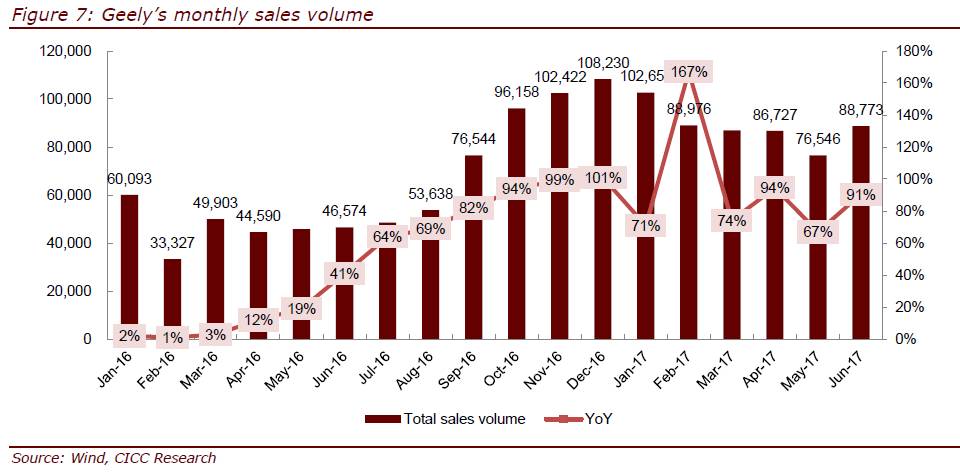

1H17 sales set new record, thanks to stronger product and brand.

Geely’s 1H17 sales volume was 530,627 (+89% YoY & +9% HoH), a new YoY growth record. Its product portfolio keeps improving and its Generation 3.0 products have helped lift Geely’s brand value. With more profitable product mix and brand premium, Geely’s sales uptrend could be maintained with enhanced GPM.

Lifting sales target shows confidence; LYNK & Co secures 2H17 momentum.

Geely raised its 2017 full year sales target to 1,100,000, showing strong confidence in its portfolio and upcoming new models. New LYNK & Co and Geely models will launch in 2H17, this strong momentum will drive the further enhancement of Geely’s profitability.

Valuation and recommendation

We are upbeat on Geely’s profitability and its growth in 2H17 with LYNK & Co as a new driver. We raise our 2017/18 earnings forecasts 12.4%/9.8% to Rmb9.0bn/13.0bn.

Maintain BUY, lift target price 25% to HK$25, implying 15.3x 2018e P/E.

Risks

Profitability of new cars misses expectations.